- Neobanks offer better products, propositions, and customer experience in a single, user-friendly app.

- Traditional banks are less agile due to evolving regulations amid technology advancements, complex legacy systems developed in another century, and heavy tech debt.

- Legacy core banking systems are one of the biggest barriers to meeting the expectations of today’s tech-savvy customers.

The banking landscape has transformed rapidly in recent years, driven by advancements in technology and the rise of digital-native consumers who increasingly expect seamless digital experiences across sectors. Neobanks and fintechs are fueling the trend by offering faster, more personalized, and user-friendly services to meet customer expectations built on modern core banking systems that enable greater agility and innovation. Innovative digital-first banks, such as Monzo, N26, Starling, and Revolut, have set new customer service benchmarks in a short period of time compared with traditional banks. Revolut, for example, was launched in 2015 and has grown to become one of the world’s largest neobanks with more than 50 million customers globally and a valuation of US$45 billion.

Neobanks have succeeded by offering simple services that traditional retail banks either did not want to offer, made too expensive or were not focused on the customer experience. They started with a different value proposition to win customers over and have scaled additional services using the same principles.

What services do modern neobanks offer?

Today, neobanks offer a range of services, including instant onboarding, mobile-first account management, instant transfers, and integrated services such as multi-currency accounts, stock and crypto trading, and budgeting tools,all within a single user-friendly app. While these capabilities have become the norm rather than the exception, they have set new benchmarks for service delivery, as customers continue to seek better benefits, reduced fees, rewards, personalized products, and faster loan approvals.

The gap between neobanks and traditional banks is reflected in The Financial Brand’s 2025 Retail Banking Trends and Priorities Report, which found that 62% of banks planned to offer real-time payments this year, up from 49% in 2024, despite the service already being provided by fintechs and neobanks. While many banks recognize the increasingly competitive nature of financial services, they remain tied to outdated core banking systems, according to The Financial Brand report. Just one quarter of respondents said they have prioritized the modernization of back-office infrastructure, even though more than half list digital experience as a strategic priority.

Banks can only fix the perception of service to a certain degree before the root cause blocks real progress. Just as you wouldn’t put a bigger engine in a Mini Cooper to win a Formula 1 race, banks need to redesign and re-build legacy systems from the ground up. Without changes to their core systems, banks will continue to fall short despite cosmetic upgrades to digital channels.

Why are traditional core systems holding banks back?

Legacy core banking systems are one of the biggest barriers to meeting the expectations of today’s tech-savvy customers. Designed years ago, many were built on rigid, monolithic architectures, which make even minor changes complex, costly, and time-consuming, according to a risk advisory firm K2 Integrity. Even updating a single product feature, for example, can require changes across multiple dependent systems and increase operational risk, the report adds.

These legacy systems often rely on batch processing, which restricts the ability to update data in real time or respond instantly to customer actions, a standard feature in digital-first banks such as Revolut. Limited API support also makes connecting with modern channels, fintech partners, and third-party platforms more difficult.

Meanwhile, a report by Accrevent found that many core banking systems continue to run on COBOL, a programming language designed in 1959. The shrinking pool of COBOL developers due to retirement means there is no new talent entering the workforce who are specialized in old tech and the coding language. As a result, banks are running code without fully understanding its function or the potential impact of changes on downstream operations, making banks vulnerable to operational risk.

One example is the outages that high street banks in the UK experienced this year, which I suspect may have been caused by legacy technology – highlighting the unacceptable impact on customers and the risk that it will be a recurring theme for banks running legacy technology. This has also increased banks’ reliance on costly, specialized contractors. At the same time, it has slowed development cycles and limited flexibility, which is no longer viable in today’s banking landscape.

Maintaining these platforms requires a large share of IT budgets, leaving fewer resources for customer-facing innovation. They also pose security risks as they are difficult to fix quickly to protect against evolving cyberattacks and regulatory compliance issues. The technological limitations also affect competitiveness, particularly when well-funded “go digital” initiatives fail because the core system remains unchanged, the K2 Integrity report says, citing HSBC’s Zing payments app, which was shuttered just one year after launch when it failed to gain traction.

“This is not an isolated case. Many traditional banks have tried to break into fintech, only to face similar challenges: slow adoption, lack of differentiation, and an inability to scale,” K2 Integrity adds.

“Too often, legacy institutions treat fintech initiatives as technology upgrades rather than business transformation strategies, overlooking the structural, operational and culture shifts needed for success.”

Even substantial investment in front-end design cannot offset back-end constraints. Without changes to core systems, banks will be unable to match the speed, agility, or personalization that customers now expect.

How do internal mindsets and governance hold back innovation?

Traditional bank culture typically focuses on stability, compliance, and risk minimization—traits that customers still value, along with service improvements. But rapid experimentation is difficult and can lead to innovations remaining in silos or pilots that fail to scale. Leadership teams can resist disruptive changes, fearing impacts on customers or operations, which slows decision-making and limits responsiveness to market shifts.

According to a McKinsey & Company report, just 30% of banks have reported successfully implementing their digital strategy, and the majority fall short of their stated objectives.

“Banks often argue that if they had a sufficient technology budget, their transformations would be successful. But we have seen several banks in recent years allocate significant resources to their digital transformations and still struggle to execute them,” McKinsey says.

Meanwhile, a study by KPMG found that only 18% of banks have successfully achieved their transformation goals.

“Rather than focusing on siloed cost and transformation initiatives, start by understanding who you want to serve, how you want to serve them, and what products and services they will need,” KPMG notes in the report.

However, banks have a history of not learning from past experiences. For example, many invested heavily in the implementation of CRM systems in the 1990s, under the pretext of offering better customer service, and failed. Had they focused more explicitly on growth in wallet share, I am convinced they would have been more successful.

Why are many banks stuck in their transformation journey?

Most bank leaders understand the need to modernize core banking systems to meet customer expectations, ensure regulatory compliance, improve operational efficiency, enhance security, and stay competitive.

However, the challenge lies in execution. Core system replacement carries high risks, is expensive, often runs over budget and takes years to complete, according to the McKinsey report. Budgetary pressures also compete with other strategic priorities, while leadership teams may hesitate to commit resources to long-term projects that do not deliver immediate returns.

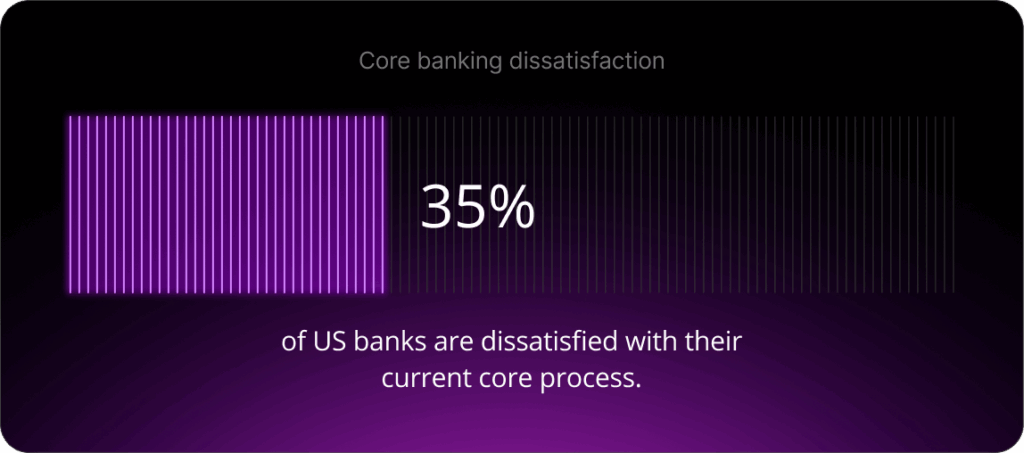

Meanwhile, the American Bankers Association’s 2024 Core Platform Survey found that 35% of US banks are dissatisfied with their current core process, while only one in five are likely to switch core providers at contract renewal. A skilled talent shortage is adding to the challenge as few internal teams have the experience needed to manage large-scale system migrations. Competition for external expertise also remains high and is driving up costs.

While banks have a high level of trust among customers, which remains an advantage over challenger banks, a failed migration or prolonged service outage can damage a bank’s reputation. Faced with these risks, many institutions have chosen the path of version updates rather than tackling the core problem, even when they know these changes will not close the competitive gap.

While this may protect short-term performance, traditional banks are increasingly vulnerable to more agile competitors, as evidenced by the rise in neobanks.

Conclusion

Banks face growing pressure to deliver the speed, agility, and personalization that customers have come to expect. Digital-first banks have set new standards, while legacy systems and the risks of large-scale change continue to hold many traditional banks back.

In the second part of our series on core banking, we explore how banks can begin the transformation process without necessarily replacing their core systems or disrupting their day-to-day operations and how this approach can improve the customer experience from the outset.

The way forward for banks is clear: They need to start thinking about core banking from a strategic viewpoint; as an opportunity rather than a risk. How can they migrate to a modern core banking system while improving customer experience – and where should they start?

Find out more. Request a demo today and see how SBS can help you to upgrade your core banking.

Questions and Answers

Core banking refers to the back-end systems that process daily banking transactions and post updates to accounts and other financial records. These systems form the technological backbone of a bank, handling everything from deposits and withdrawals to loan processing and account management. Core banking matters because it directly impacts a bank’s ability to serve customers efficiently, launch new products quickly, and compete with digital-first challengers.