- Growth opportunities remain, but organizations face a new operating reality this year.

- Asset finance providers are shifting their focus from scale to resilience in 2026.

- The sector is moving to formalize AI oversight, maintain model inventories, and ensure human control over high-impact decisions.

Asset finance has started 2026 on a relatively positive note. Global equipment and automotive finance markets are continuing to grow, while demand for financing remains resilient across most regions. However, operating conditions are becoming more complex, and volatility remains, albeit in a different form. Throughout 2025, asset finance firms had to navigate a range of headwinds, including macroeconomic uncertainty, sticky inflation in some markets, supply chain disruptions, rising cyber risks and increasingly assertive regulations, according to the SBS Asset Finance in 2026: Trends and Innovations report.

At the same time, technology capabilities – particularly in data, artificial intelligence and platform integration – matured rapidly. What was experimental only a few years ago is now expected to operate at scale, under more regulatory scrutiny and with measurable business impact.

In 2026, the asset finance sector is expected to be defined by disciplined execution rather than headline growth. Real-time data and dynamic decisioning will become increasingly important, while AI will move from an advantage to a necessity, and operational resilience will emerge as the true differentiator.

Why precision matters in 2026

As the report notes, growth opportunities remain in 2026. Infrastructure investment, fleet renewal, and the expansion of digital and used-asset financing continue to support demand. Markets such as India and Mexico will continue to attract manufacturing investment, driving demand for equipment and fleet finance. However, the growth is expected to become uneven this year. High interest rates, inflationary cost pressures, and tariff volatility are increasing the cost of capital and complicating asset pricing and residual value assumptions, according to the report.

Meanwhile, supply-chain disruptions will continue to affect delivery timelines, while trade policy and tariff volatility will impact asset pricing, residual value assumptions, and contract structures, particularly for cross-border transactions. This has resulted in asset finance providers shifting their focus from growth to resilience. Technology investments are increasingly directed toward protecting margins, improving decision quality, and reducing operational friction rather than simply driving origination volumes.

This means that asset finance managers will have to navigate uncertainty with precision by combining selective growth with operational discipline, stronger risk frameworks, and technology capabilities designed to manage complexity rather than assume uniform conditions.

How data has become the operating system of asset finance

Most asset finance organizations hold decades of data across origination, servicing, asset management, and remarketing. Yet much of this information remains fragmented, locked in legacy systems, and used primarily for hindsight rather than foresight.

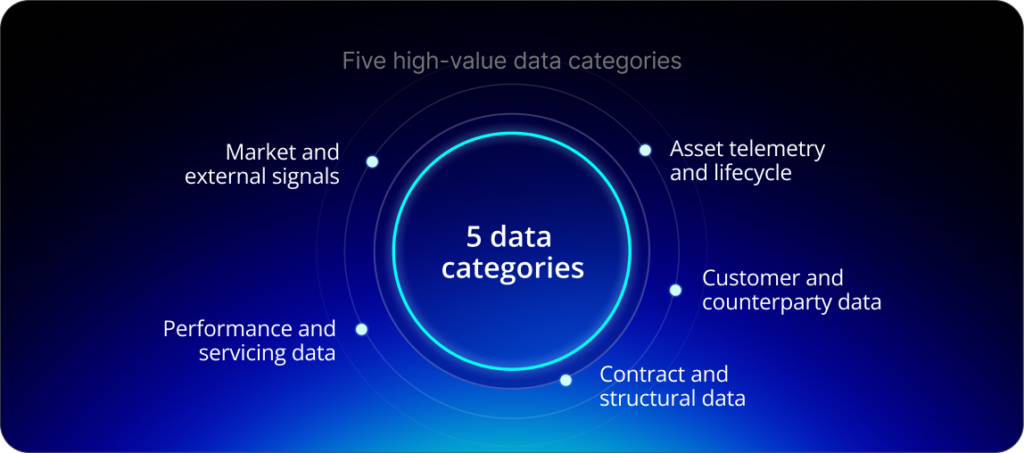

The challenge is not data availability, but data usability. Wholesale and floorplan providers typically hold five categories of high-value data:

- Contract and structural data.

- Performance and servicing data.

- Customer and counterparty data.

- Asset telemetry and lifecycle data.

- Market and external signals.

When combined, these datasets enable predictive analytics, early warning indicators, and more accurate pricing and exposure management. Leading firms are prioritising consolidation of high-impact data sources into cloud-based platforms and focusing on a small number of models – notably early portfolio risk indicators and residual value predictors – embedded directly into operational workflows.

The impact is measurable. Predictive analytics have been shown to improve forecast accuracy by 20% to 25% in mature implementations.

Why AI has moved from an advantage to a necessity

AI has moved from being an experimental technology in asset finance, with adoption accelerating across three high-impact domains:

- Credit decisioning: Structured and unstructured data is used to improve accuracy and speed.

- Predictive analytics: To support dynamic pricing, provisioning, and exposure management.

- Dealer and fleet scoring: To enable differentiated limits and pricing.

As AI continues to grow in popularity, regulatory scrutiny is also increasing. For example, the European Union’s AI Act focuses on explainability, transparency, and governance. This has resulted in organizations formalizing their AI oversight, as well as maintaining model inventories and ensuring that humans oversee high-impact decisions.

By the end of 2026, the question will no longer be whether AI is used, but how effectively it is governed and embedded into daily operations.

“The challenge is not data availability, but data usability, bringing siloed data together in a way that enables explainable, secured, sovereign AI insights and action, under full human control,”

Hani Hagras, Chief Science Officer and Global Head of AI at SBS, notes in the report.

How cybersecurity has become a balance-sheet issue

In 2025, numerous cyber breaches highlighted how they can impact supply chains, causing major disruptions to manufacturers, dealers, service providers, and the financiers that support them.

Cybersecurity has shifted from a technical concern to a strategic and financial risk.

In response, regulators are strengthening expectations around operational resilience, third-party oversight, and incident response. Company boards are also expected to demonstrate oversight of cyber risks and recovery planning, as well as treat cybersecurity investment as a protection against risk rather than a balance-sheet issue.

Why cross-border capability will accelerate in 2026

Cross-border origination and asset deployment are expected to accelerate this year, fuelled by a realignment in supply chains, nearshoring, and uneven regional growth. Tariffs and export controls are also expected to impact asset costs and delivery timelines.

To maintain control as assets move across jurisdictions, asset finance firms are now embedding cross-border considerations earlier in the credit lifecycle, refining underwriting, contract design, and asset monitoring.

Looking ahead

For asset finance organizations, the challenge in 2026 is no longer identifying growth opportunities but executing them with precision in an increasingly volatile economic landscape. As real-time data, AI, and dynamic decision-making continue to merge with core operating systems, organizations will be able to build resilience to navigate uncertainty. Download the full Asset Finance in 2026: Trends and Innovations report here.

Questions and answers: Asset finance today

While growth in the sector continues, it has become more uneven, driven by a range of economic headwinds, such as macroeconomic uncertainty, sticky inflation in some markets, supply chain disruptions, rising cyber risks, trade policies, and rising tariffs.