- Mobile internet users are projected to reach 5.5B by 2030, up from 4.7B in 2024, expanding the mobile banking user base.

- Smartphones are projected to account for 91% of global mobile connections by 2030, up from 80% in 2024.

- The total value of digital wallet transactions is expected to grow 77% to over US$16T by 2028, signaling deeper mobile banking adoption.

Mobile banking has revolutionized how people manage their finances in real-time, driven by innovative advancements in app development, open-banking APIs, and high-speed Wi-Fi connections. Agile fintechs are at the forefront of the mobile banking revolution as they accelerate technological advancements in the sector and introduce cutting-edge features that retail banks are increasingly integrating into their platforms to remain competitive. These innovations, including peer-to-peer (P2P) payments, biometric authentication, and artificial intelligence (AI), have significantly enhanced security and created seamless user experiences. “Mobile is now the gateway to everyday banking for a growing majority of consumers in various markets,” McKinsey and Company says in its State of Retail Banking report. “Banks, therefore, need to design their distribution so it leads with mobile.”

How has consumer behavior changed in mobile banking?

Mobile banking first emerged in 1999 with basic services, such as balance inquiries, offered through SMS channels. However, the behavior of consumers was transformed during the COVID-19 pandemic, as millions of people worldwide worked from home during lockdowns.

Today, consumers expect real-time access to financial services. They want hyper-personalized experiences that let them automate bill payments, set savings goals, invest, and budget, among other features. The demand for convenience and customization has never been higher.

A 2024 survey by Q2 Holdings found compelling statistics about modern banking preferences:

- 74% of consumers across generations want more personalized experiences from their banks

- 48% log into their mobile banking apps or websites daily

- 48% of consumers demand higher security

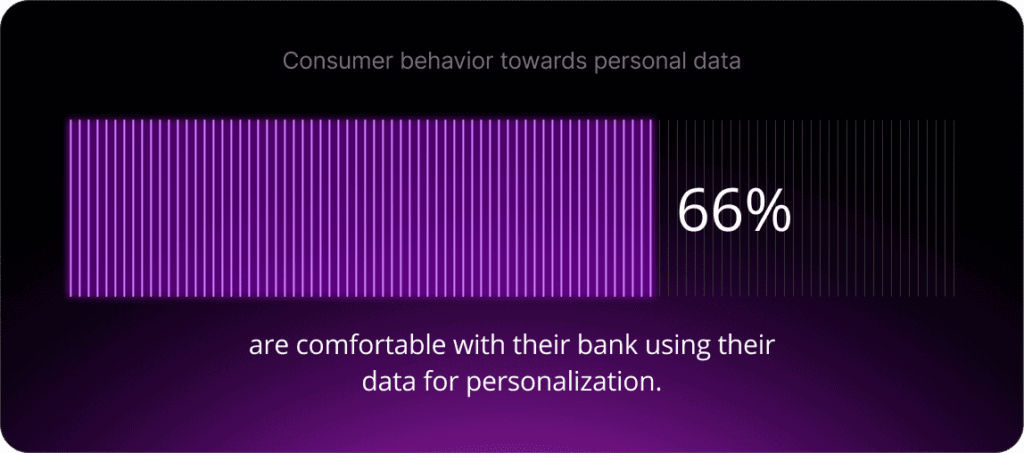

- 66% are comfortable with their bank using their data to personalize their experiences

“The digital landscape is continuing to shift and evolve for banks and credit unions,” says Anthony Ianniciello, Q2’s vice president of product management. Consumers across all generations are asking for the same things: personalized experiences, increased security, and an increased use of AI.

What role does smartphone penetration play?

The global penetration of smartphones has also been a significant driver of the expansion of mobile banking in the financial ecosystem. Since 2023, smartphone usage has surged, enabling banks to reach a broader customer base, including unbanked or underbanked populations.

GSMA statistics show that the number of people using mobile internet reached 4.7 billion in 2024, representing 58% of the global population, and is projected to grow to 5.5 billion users by 2030.

GSMA also notes that smartphones accounted for around 80% of global mobile connections in 2024, a share projected to rise to 91% by 2030, confirming that smartphones have become the dominant access point to mobile internet worldwide.

Smartphone penetration is no longer a competitive advantage, it is a baseline condition. What matters now is how effectively banks use mobile as a platform to deliver value, intelligence, and trust. The real differentiators lie in what happens on top of the device: AI-driven experiences, secure digital identity, and seamless service integration.

Transformative impact on personal finances

The convenience of 24/7 access, intuitive interfaces, and customized services have reshaped customers’ expectations. Features such as instant transfers, mobile deposits, and easy bill payments are now the norm, allowing customers to manage their finances seamlessly.

However, hyper-personalization, which leverages AI and machine learning data analytics to tailor services to individual preferences, has significantly enhanced the overall customer experience. It has set a new standard in the industry through personalized products, tailored financial advice, and real-time financial solutions.

“As consumers increase their use of digital banking services, they grow to expect more, particularly when compared to the standards they are accustomed to from leading consumer-internet companies,” McKinsey says.

How do banks benefit from operational efficiency?

Financial institutions that embrace mobile banking have reduced operational costs associated with maintaining physical branches. AI has also enabled them to automate routine tasks, allowing employees to focus on more important strategic responsibilities.

According to McKinsey, banks adopting a mobile-first integrated distribution strategy have also increased deposit balances by 10% to 15% by optimizing their distribution channels. This efficiency lowers costs and enables banks to allocate resources to enhance digital platforms and customer service.

What are current consumer preferences?

Understanding and meeting consumer expectations is paramount in the mobile banking revolution. While personalization is a key factor driving user adoption, others include:

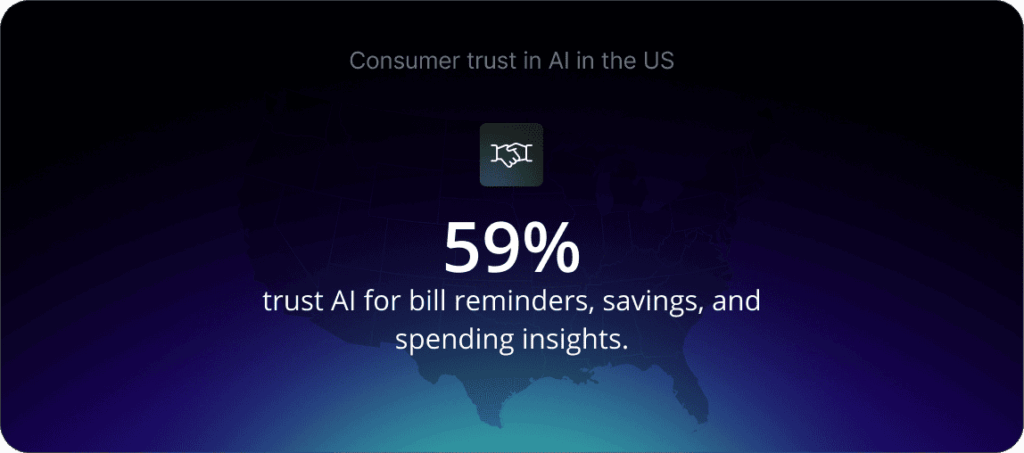

- Trust in technology: A survey by MX Technologies found that more than half (59%) of US consumers trust AI to deliver proactive reminders to pay bills, save money, and provide a comprehensive breakdown of their spending.

- Seamless integration: 57% of consumers would link all their finances into a single mobile app if given the option, according to MX Technologies. This is despite many financial institutions offering this feature on their mobile banking apps.

- Financial education and insights: Almost half (42%) of US consumers want educational programs to help them become financially stronger, and 33% are seeking predictive insights and personalized recommendations to manage their finances better, the MX Technologies study found.

Which innovations are shaping mobile banking?

Numerous innovations are transforming mobile banking. These include:

Mobile wallets and contactless payments

The rise of mobile wallets such as Apple Pay and Google Pay has transformed consumer spending habits by enabling contactless payments. Digital wallets offer a secure and convenient way to conduct transactions, further embedding mobile banking into consumers’ daily lives.

According to Juniper Research, the total value of digital wallet transactions is expected to jump by 77% from US$9 trillion in 2023 to over US$16 trillion by 2028. The trend is being driven by growth across developed and developing markets thanks to services such as Buy Now, Pay Later, microloans, and personal finance management tools, Juniper adds.

Agentic AI: from virtual assistants to early autonomous capabilities

Forrester’s 2024 European Digital Experience Review highlights that banks are evolving from basic chatbots to sophisticated virtual assistants that anticipate customers’ needs.

“As AI evolves, we expect digital banking experiences to become increasingly seamless and immersive, transforming the app from a transactional tool into a trusted advisor—revolutionizing how customers interact with their banks,” Forrester says in the report.

Agentic AI represents the next step in this evolution. While still emerging, McKinsey & Company notes that some leading banks are already piloting agentic AI systems in frontline activities such as prospecting and lead nurturing, as well as other customer-facing functions. As these capabilities mature, they are expected to inform future mobile banking experiences, enabling more proactive and intent-driven interactions without removing human oversight.

Super apps: from banking apps to everyday platforms

Open-banking APIs facilitate the connection of various financial tools and services through third-party fintechs. This enables banks to offer their customers a more comprehensive and integrated solution on a single platform by allowing fintechs to access their financial data.

Building on this foundation, the financial super app has already emerged as one of the most promising evolutions of mobile banking. Super apps integrate multiple services into a single platform, including banking, payments, investing, insurance, and personal finance management, and in some cases extend beyond financial services altogether.

This holistic approach enhances convenience and fosters deeper customer engagement by addressing both financial and everyday needs within one mobile experience. By evolving toward super app models, banks can position their mobile platforms as indispensable tools in customers’ daily lives, strengthening loyalty and expanding their service offerings. Examples of super apps include Paytm in India, Alipay and WeChat in China, GCash in the Philippines, and Gojek in Indonesia. In Europe, Revolut is also moving in this direction, progressively adding services such as travel bookings, communications features, and subscription offerings alongside core banking services.

What role does digital identity play in mobile banking?

Digital identity (ID) systems are fast becoming an essential element to future-proof global economies, allowing citizens to securely access a range of public and private platforms to carry out everyday activities, from banking and healthcare to paying taxes and signing documents. In the banking sector, digital IDs offer users more secure and inclusive financial services, streamline customer onboarding, verify mobile banking transactions, reduce fraud, and enhance customer support channels.

Several countries have already demonstrated how digital identity can be embedded at scale within banking ecosystems. Sweden’s BankID, is playing a key role in the day-to-day delivery of financial services, allowing customers to log into mobile banking apps, authorise payments, sign credit agreements or apply for loans, thanks to its digital signature feature.

At a European level, this approach is now being formalised through eIDAS 2.0 (Regulation (EU) 2024/1183), which establishes a framework for European Digital Identity Wallets. According to the regulation, the European Digital Identity “will be available to EU citizens, residents, and businesses” and “can be used for both online and offline public and private services across the EU.”

What does the future hold for mobile banking?

Emerging technologies such as 5G, the Internet of Things (IoT), and augmented reality (AR) will shape the future of mobile banking, making interactions immersive and even more seamless than they are today. AI will continue to play a pivotal role in the future of mobile banking by transforming apps into comprehensive financial advisors that offer customers personalized financial guidance.

Mobile banking has revolutionized the financial industry by improving accessibility, efficiency, and customer personalization. The adoption of advanced technologies and strategies such as mobile-first distribution and hyper-personalization has allowed banks to strengthen customer relationships and broaden their scope. As mobile banking progresses, financial institutions that prioritize innovation and invest in technology and analytics will be well-positioned to shape the future of finance.

For more expert content on industry outlooks and innovation, subscribe to our newsletter or visit our Insights page.

Questions and Answers

The main mobile banking trends heading into 2026 include hyper-personalised, AI-driven experiences, the rise of financial super apps, deeper integration of digital identity, and the shift toward mobile-first distribution models. Banks are increasingly using AI to deliver proactive insights, automate financial tasks, and anticipate customer needs, while open-banking APIs enable broader service ecosystems within a single app.