- International card schemes like Visa and Mastercard account for roughly two-thirds of card transactions across the euro area.

- Big Tech platforms such as Apple Pay and Google Pay increasingly control the customer payment interface.

- European authorities are focused on rebuilding a public, interoperable payments backbone to defend payment sovereignty.

Europe is at risk of losing control over how money moves in the digital economy. The infrastructure that processes everyday payments in the euro zone is now largely dominated by international card schemes, global technology platforms and emerging private digital currencies.

In response, European institutions are undertaking a structural overhaul of payments and settlement infrastructure, centred on the digital euro, the expansion of real-time payment rails and the modernization of systems to support tokenized finance. Over the coming years, these initiatives will reshape how money circulates across Europe and fundamentally alter the role of banks within the payments ecosystem.

The erosion of payment sovereignty

The question of European payments sovereignty is not a new one. For decades, Europe has struggled to build pan-European payment schemes capable of scaling across borders. While several domestic solutions have emerged over time, only a handful, such as iDEAL in the Netherlands and Paylib in France, have achieved meaningful adoption. These successes, however, remain confined within national borders. Europe’s payments landscape continues to be characterized by fragmentation, with a patchwork of domestic schemes, clearing systems and banking infrastructures developed independently over decades.

This fragmentation has created space for global players to fill the gap. International card schemes such as Visa and Mastercard now dominate digital retail payments, accounting for roughly two-thirds of card transactions across the euro area. At the same time, Big Tech platforms such as Apple Pay and Google Pay increasingly control the customer payment interface, shaping user behaviour and capturing valuable transaction data on top of existing card rails.

The next wave of financial digitalization risks accelerating this trend even further. Tokenized assets, programmable payments and private stablecoins are beginning to introduce new settlement layers that operate outside traditional banking systems. If widely adopted, these privately governed digital infrastructures could further displace European payment rails, shifting both value storage and transaction flows beyond public and European oversight.

Why does payment sovereignty matter?

At first glance, the dominance of international card schemes and global payment platforms may appear primarily as a commercial issue. After all, European consumers enjoy seamless digital experiences, and merchants benefit from near-universal acceptance. However, the gradual shift of payment infrastructure beyond European governance carries deeper strategic, operational and economic consequences.

From a resilience and security standpoint, reliance on externally governed payment networks creates structural vulnerability in a critical layer of the financial system. Payments infrastructure is no longer a neutral utility but a strategic asset that shapes standards, access and technological direction. Concentration around a small number of global platforms increases systemic risk and constrains Europe’s ability to guarantee continuity of financial flows in times of crisis or geopolitical tension.

The economic implications are also significant. Outsourced payment infrastructure channels transaction fees, platform revenues and increasingly valuable payment data outside the euro area. As digital payments grow and new data-driven financial services emerge, these flows represent not only immediate costs for European merchants and banks, but also a long-term transfer of strategic value.

Over time, this dynamic risks weakening Europe’s financial ecosystem. Domestic institutions become increasingly dependent on external platforms for distribution and customer access, while investment, technological leadership and pricing power accumulate elsewhere. What begins as convenience gradually evolves into structural reliance.

As noted by Piero Cipollone, Member of the European Central Bank’s (ECB) Executive Board, in his recent speech on Europe and monetary sovereignty, “If we lose control of our money, we lose control of our economic destiny. And we surrender a key attribute of sovereignty.”

Europe’s infrastructure-led response

Europe’s response to this issue has been deliberately structural. Rather than attempting to limit the role of global platforms through rules alone, European authorities are focused on rebuilding a public, interoperable payments backbone capable of anchoring digital finance in European-governed infrastructure. At the centre of this strategy sits the ECB, working alongside national central banks and market participants to modernize both retail and wholesale settlement layers.

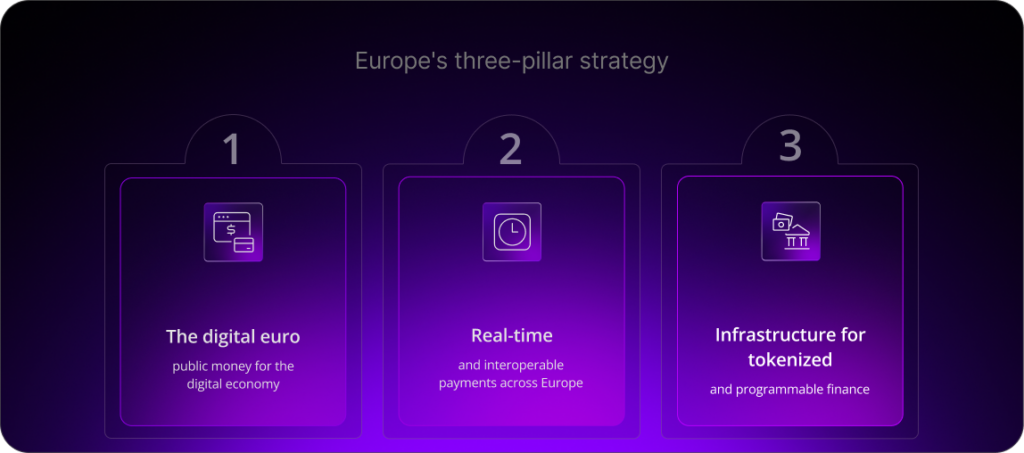

This infrastructure-led approach rests on three core pillars.

The digital euro: public money for the digital economy

The digital euro is the proposed retail central bank digital currency of the ECB. It would introduce a digital form of public money, available alongside cash and bank deposits, and usable for everyday payments across the euro area.

In essence, it would function as digital cash: a direct claim on the central bank, universally accepted and settled in central-bank money. The project has moved from investigation into a preparation phase focused on technical design and legislative alignment. Final political approval is still pending and large-scale rollout is unlikely before the latter part of the decade, though in March 2026 the Eurosystem opened a call for payment service providers to participate in a 12-month pilot scheduled for the second half of 2027. Rather than replacing private payment services, the digital euro is intended to operate through supervised intermediaries, including banks, which would distribute it to customers and integrate it into existing payment interfaces.

By anchoring digital transactions in public money, the initiative seeks to preserve European control over the core monetary layer as payments become increasingly digital and programmable.

Real-time and interoperable payments across Europe

In recent years, Europe has been accelerating the rollout of instant settlement infrastructure to enable real-time payments across borders. These rails allow funds to move between accounts in seconds, 24 hours a day, reducing friction, cost and reliance on international card networks. Crucially, real-time infrastructure also helps overcome Europe’s fragmentation problem. By providing a common settlement layer across markets, it enables European payment solutions to scale continent-wide rather than remaining confined to national ecosystems.

Initiatives such as Wero illustrate how banks are beginning to translate this infrastructure into market-facing alternatives, offering pan-European account-based payments without dependence on foreign card schemes or Big Tech wallets.

Infrastructure for tokenized and programmable finance

The ECB and several national central banks have already begun conducting wholesale experiments linking distributed ledger platforms to central-bank settlement systems. These trials have focused on issuing and settling tokenized bonds, exploring delivery-versus-payment models and testing how existing TARGET services can interoperate with new digital infrastructures.

At the same time, major European banks are working on tokenized deposit models as an alternative to private stablecoins, seeking to ensure that bank money remains competitive in digital asset environments. Regulatory frameworks such as MiCA are also bringing stablecoin issuers under EU supervision, limiting the risk of unregulated private settlement layers gaining dominance.

As financial markets digitize and become programmable, Europe wants central-bank money and supervised bank liabilities to remain at the core of settlement, rather than private tokens issued outside the banking system.

| Today | Where Europe Is heading | |

| Payment infrastructure | Dominated by international card schemes and global platforms | Development of European-governed rails, including instant payments and digital public money |

| Market structure | Fragmented national systems | Greater interoperability and euro-area-wide settlement |

| Digital innovation | Big Tech and private digital currencies shaping payment interfaces | Public infrastructure combined with regulated digital asset frameworks |

| Role of banks | Dependent on external networks for distribution and settlement | Central intermediaries in distributing and integrating new European infrastructure |

| Strategic objective | Operational efficiency with structural dependence | Greater resilience, sovereignty and balance between public control and private innovation |

Challenges in implementation

Europe’s infrastructure-led strategy is commendable, but it also poses challenges in implementation. Rebuilding sovereignty in payments is not simply a technical upgrade; it requires behavioral change, business-model adjustment and regulatory alignment across a fragmented euro-area landscape.

The infrastructure can be built. The harder question is whether the ecosystem will realign around it.

Adoption

Payment systems are governed by network effects. Consumers use what is widely accepted and frictionless, and merchants support what customers already demand. A digital euro or European payment alternative must therefore overcome entrenched dynamics:

- Consumer habit inertia

- Merchant reluctance to invest in new acceptance infrastructure

- Switching costs embedded in long-term acquiring and processing contracts

- The convenience, scale and brand advantage of dominant global platforms

- The embedded consumer protection frameworks of existing card schemes, including dispute resolution, chargebacks and well-established fraud liability models

Without rapid accumulation of critical mass, even technically sound European solutions risk remaining complementary rather than transformative.

Integration model with banks

European banks are central to the distribution and integration of new public infrastructure. The digital euro model relies on banks and payment service providers to interface with customers, while instant settlement and tokenized platforms depend on bank-level system upgrades.

However, this transition introduces structural tensions:

- Potential compression of card-related issuing and acquiring revenues

- Possible shifts in deposit dynamics if digital public money affects liquidity behavior

- Migration of certain payment economics or customer interface control

- Significant investment requirements to modernize legacy core systems

For some institutions, particularly those with aging infrastructure, integration complexity may be substantial.

Regulatory coordination

Payments reform cuts across multiple regulatory domains: digital assets, banking supervision, consumer protection, data governance and competition policy. Legislative processes for central-bank digital currency, stablecoin oversight and instant payment mandates must align across EU institutions and national authorities.

Fragmentation at the regulatory level could undermine harmonization at the infrastructure level. Clear governance, predictable supervisory frameworks and consistent standards will be essential if new payment rails are to achieve pan-European scale.

What this means for European banks

European banks sit at the center of this transformation. The emerging payments architecture is designed to operate through supervised intermediaries. Banks will distribute digital public money, integrate new settlement rails and shape the customer-facing layer of Europe’s next-generation payments ecosystem. At the same time, the balance of power within payments is shifting. Traditional revenue streams linked to card issuing and acquiring are under pressure. Control of the customer interface is increasingly contested. Liquidity, data and platform positioning are becoming strategic variables rather than operational details.

The challenge for Europe is therefore not to replace private innovation with public control, but to rebalance the system. Public infrastructure must ensure resilience, sovereignty and long-term stability. Private institutions must continue to drive innovation, competition and customer experience.

Achieving this balance between public sovereignty and private innovation will require coordinated transformation across the financial ecosystem. SBS support this shift by combining deep banking expertise with large-scale technology and integration capabilities, helping European banks modernize payments infrastructure while remaining resilient, compliant and competitive in a rapidly changing environment.

For more expert content on industry outlooks and innovation, subscribe to our newsletter or visit our Insights page.

Questions and answers: Payment sovereignty in Europe

Payments sovereignty refers to Europe’s ability to control the infrastructure, governance and settlement mechanisms through which the euro moves in the digital economy, not just the currency itself.