- 86% of companies in France have experienced late payments, while more than 50% say the impact on their cash flow is critical.

- In the first eight months of 2025, 42,505 failures were recorded, a record level that exceeds the pre-Covid level by 37%.

- Advanced generative AI capabilities can improve recovery rates by about 10% and reduce operational costs by up to 40%.

Recovery teams at banks and financial institutions in France are facing surging collection volumes as businesses and households cope with tighter cash flows amid ongoing economic uncertainty. Adding to the pressure is the country’s challenging payment landscape. According to a 2025 Coface payment survey, 86% of companies in France have experienced late payments, while more than 50% say the impact on their cash flow is critical. “Even more worrying is that 42% of companies attribute these delays to the financial difficulties of their customers, revealing a vicious circle that weakens the entire economic fabric,” Coface notes. This deterioration is reflected in a “continuous increase in insolvency rates: in the first eight months of 2025, 42,505 failures were recorded, a record level that exceeds the pre-Covid level by 37%,” Coface adds. AI collection tools are emerging as a key response to this pressure.

Meanwhile, Banque de France data shows that corporate defaults jumped 18% to reach 65,000 in 2024, while a report by Groupe BPCE estimates that 69,000 French businesses were expected to fail in 2025. As payment delays and insolvencies increase, recovery teams are managing higher collection volumes while operating within tight cost and regulatory constraints. Maintaining recovery rates and customer standards without increasing headcounts has become more difficult, particularly for financially fragile customers who require careful handling. This is leading some banks and financial institutions to shift away from manual workflows in collections toward more automated and predictive models designed to stabilise performance.

According to a report by Markets and Markets, the AI in finance market is projected to grow from US$38.3 billion in 2024 to US$190.3 billion by 2030, representing an impressive compound annual growth rate of 30.6%. As investment in AI rises, research by McKinsey estimates that advanced generative AI capabilities in customer assistance and collections can improve recovery rates by about 10% and reduce operational costs by up to 40%. It can also lead to an increase in customer satisfaction of up to 30%, McKinsey adds.

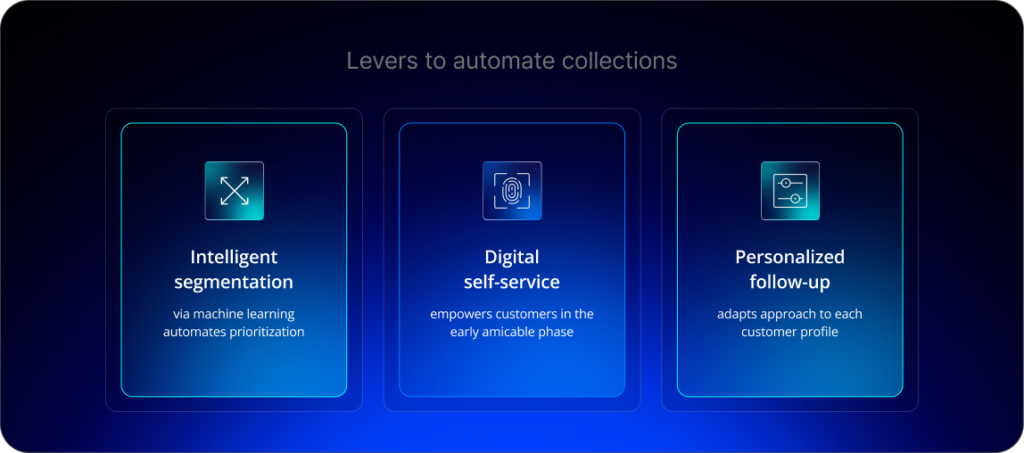

Three levers are key to automating collection processes

Three levers have emerged as central to automating and industrializing collection processes in France. The first is intelligent segmentation to automate prioritization, followed by digital self-service to empower customers during the early stages of payment delinquency. The third lever is based on personalized follow-up strategies.

Intelligent segmentation via machine learning automates prioritization

- AI analyzes behavior, payment history, and signals to predict the probability of repayments.

- It automatically segments cases by priority, risk, and recommended action.

- AI identifies self-cure customers who don’t need intervention.

- It frees analysts from manual triage and prioritization work.

Digital self-service empowers customers in the early amicable phase

- After AI-based segmentation, and in accordance with strategies defined by collections teams, customers can be directed to digital channels, allowing them to manage their situation independently.

- Payment plans, reminders, and options are available 24/7 without agent intervention.

- Digital self-service reduces inbound calls and manual interventions for routine cases.

- This lever is particularly important for fragile customers who prefer discreet digital solutions.

Personalized follow-up adapts approach to each customer profile

- After AI segmentation, bank employees can decide and tailor the communication with the right messages, channels, and tone.

- This means there are different approaches for temporary fragile customers compared to chronic non-payers.

- It also provides empathetic, supportive messaging for customers financially affected by various crises.

- AI provides insights for better human decision-making where appropriate.

AI in practice: How SBS Collection Management operationalises these levers

With SBS Collection Management, these approaches are supported by embedded AI capabilities that automate segmentation and prioritization while preserving human oversight. Rather than driving decisions, AI provides actionable insights that help collection teams adapt their follow-up strategies, absorb rising volumes, and improve recovery performance without increasing headcount.

Transforming operations through AI collection

Combined, these three levers can transform both operational efficiency and customer relationships. This is supported by research from McKinsey, which shows that a digital-first collections strategy can create value, as customers are now more comfortable using digital strategies. This suggests that “lenders that provide smarter, more interactive, and more personalized services will perform better than their less responsive peers,” McKinsey notes in the report.

“Some have seen reductions in nonperforming loans of 20 to 25%, alongside huge cost takeouts (and related increases in productivity), lower conduct risk, and more than 25% boosts to customer engagement. One lender shortened its average repayment time by as much as five times,” McKinsey adds.

By automating prioritization and enabling different communication approaches, banks and financial institutions can support fragile customers with empathetic, appropriate engagement, while applying a firm but fair approach where necessary.

In turn, this frees up team members to focus on high-value, high-stakes cases while simultaneously improving recovery rates and supporting vulnerable customers. They can also enhance the reputation of collection teams by boosting the net promoter score (NPS) and strengthening customer loyalty in a challenging acquisition and retention environment.

Platforms such as SBS Collection Management support this differentiation through automated segmentation and structured follow-up strategies. Designed to operate within France’s regulatory environment, including meeting GDPR requirements and consumer protection regulations, the software supports traceability and governance, as well as retaining human oversight for fragile customers.

A sustainable operating model

For the banking and financial sector, the message is one of urgency and practicality, as traditional manual approaches by collection teams come under increasing pressure. Automation can lift the burden of overwhelming and repetitive work, allowing collection teams to help more customers while focusing on high-value work where human judgment truly matters.

It should also be noted that AI automation is not a futuristic theory. Instead, it is a viable way to handle today’s rising volumes with existing resources. It also offers the dual benefit of not having to choose between efficiency and empathy, as automation enables both at the same time.

The result is a more sustainable operating model – one that improves outcomes, reduces burnout, and turns collections from an overworked back-office function into a structured, relationship-focused operation.

How SBS can help

SBS Collection Management is a 360-degree digital and data-driven solution for recovery operations, enabling automation and intelligent segmentation through machine learning and personalized customer follow-up. The software enables recovery services to reorganize in the face of crisis-driven volume increases without having to hire more staff.

Questions and Answers: Five key questions on automation in collection management

In France, collections teams are facing an overwhelming number of caseloads amid rising insolvencies and late payments. As increasing headcounts is not an option, automation can ease the burden and free up employees to focus on high-value, high-stakes cases while simultaneously improving recovery rates, supporting fragile customers, and strengthening customer loyalty in a difficult acquisition and retention environment.