- Collection models across the region were designed for low-default environments and relied heavily on manual processes to manage debt collection.

- Weak and fragmented recovery processes have resulted in the region’s NPL ratio reaching 8% to 9%.

- Tier 3 and Tier 4 banks face the greatest challenges when it comes to collections management.

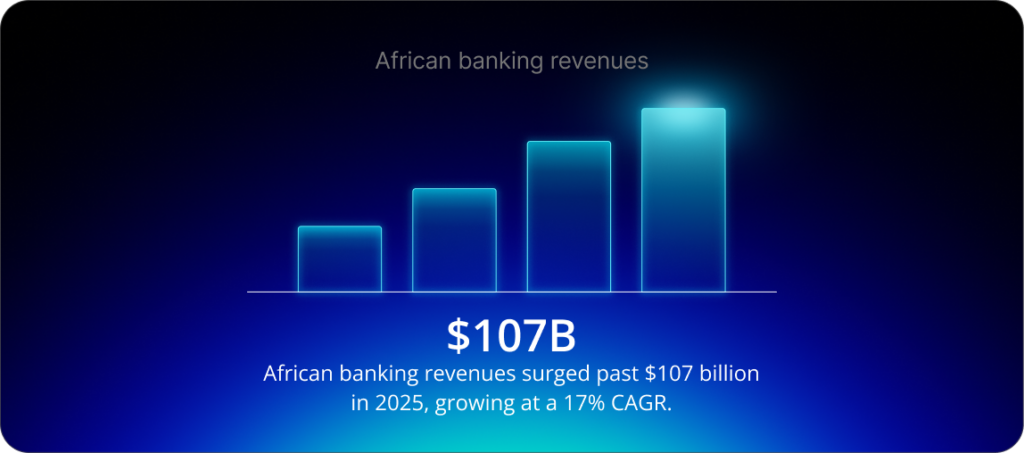

A sustained credit expansion has taken hold across North, West, and Central Africa, driven by rapid growth in SME lending and retail borrowers entering the formal financial system for the first time. African banking revenues surged past $107 billion in 2025, growing at a compound annual growth rate (CAGR) of 17% between 2020 and 2024, more than twice the global rate of 7%, according to a report by McKinsey & Company. SME lending is the fastest-growing segment and is expected to rise at a CAGR of 8% to 10% through to 2030, McKinsey adds. As lending accelerates, collections management is coming under growing pressure.

For years, low default levels meant that amicable and legal collections were often managed manually, with strong human oversight. However, a rising risk appetite, economic volatility, and security concerns have fuelled an increase in delinquency rates, giving rise to operational challenges for financial institutions.

IMF data compiled by the World Bank highlights that “weak and fragmented recovery processes” are a key reason for persistent non-performing loans (NPLs) in Sub-Saharan Africa. According to the data, the NPL ratio has reached 8% to 9% in the region compared with 2% to 3% in Western Europe. While pressure on financial institutions is mounting, smaller Tier 3 and Tier 4 banks are facing the greatest challenges when it comes to collections management. Operating at cost-to-asset ratios already double the global average, they continue to rely on a collections management process built for a different era, according to the McKinsey report.

Automation in practice: How SBS Collection Management operationalizes these levers

In recovery, SBS Collection Management supports automated segmentation, case prioritization, and action orchestration across amicable and legal collections. It enables banks to focus on human intervention on high-risk or sensitive cases while automating repetitive tasks, improving productivity, consistency, and customer engagement across growing portfolios.

Automation in collections management

Historically, collection models in Africa were designed for low-default environments and relied solely on manual processes to manage debt collection. Inconsistent case handling across legal recovery phases extends resolution timelines and increases credit losses. Combined with a lack of consolidated customer data and credit histories, a core operational weakness in African banking, the collections model is less reliable, resulting in agents relying on incomplete information, which is reflected in outcomes.

In contrast, automation offers a direct solution to the issue. In general, large-scale automation deployed by banks can reduce annual costs by up to 30% in certain functions, McKinsey notes in its Transformative Power of Automation in Banking report.

“McKinsey sees a second wave of automation and AI emerging in the next few years, in which machines will do up to 10% to 25% of work across bank functions, increasing capacity and freeing employees to focus on higher-value tasks,” the company adds.

For the collections segment alone, the gains are greater: up to 40% lower operational costs, 10% higher recovery rates, and a 30% improvement in customer satisfaction levels, as well as building long-term trust, a separate McKinsey report states. This is “driven by the technology’s ability to better identify and address customers’ needs on time, helping them to become debt-free more quickly,” McKinsey says.

How automation transforms collections processes

Automated segmentation classifies incoming cases by risk profile, outstanding balance, customer history, and behavioral signals, while prioritization directs agents’ attention to accounts where intervention is most likely to be effective.

This allows agents to focus on high-risk or sensitive cases while automating repetitive tasks, improving productivity, consistency, and customer engagement across NPL cases. Agents are not removed from the process. Instead, they are redirected toward the cases where judgment, empathy, and negotiation skills produce outcomes that automation cannot. The result is a collections function that scales with portfolio growth and can continue to handle the volume the region’s continued credit expansion is expected to generate.

Why automation is a strategic imperative for mid-sized lenders

For Tier 3 and Tier 4 banks across North, West, and Central Africa, the question is no longer whether to modernize collections processes. Instead, it is whether the current, outdated collections model can sustain the next phase of credit growth and at what cost to recovery outcomes and customer relationships?

Rising delinquency rates are not a temporary challenge. They are a structural consequence of the rapid credit expansion that African banks have actively and successfully pursued. Financial institutions that treat the modernization of their collections model as a strategic enabler will be better positioned to sustain the growth they have already achieved.

How SBS can help

SBS Collection Management is a 360-degree digital and data-driven solution for recovery operations, enabling automation and intelligent segmentation through machine learning and personalized customer follow-up. The software enables recovery services to reorganize in response to crisis-driven increases in volume without hiring more staff.

Q&A: Key questions on collections management in Africa

According to IMF data compiled by the World Bank, weak and fragmented recovery processes, which are typically managed manually, are one of the main reasons for persistent non-performing loans (NPLs) in Sub-Saharan Africa. According to the data, the NPL ratio has reached 8% to 9% in the region compared with 2% to 3% in Western Europe.