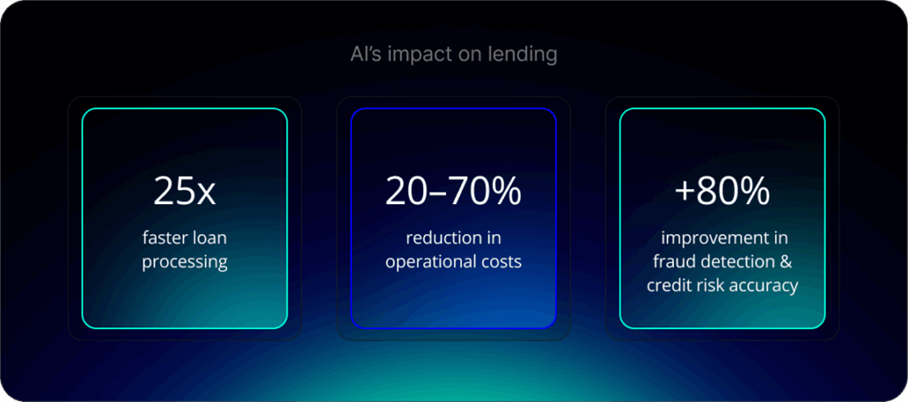

- Loan processing is up to 25 times faster and operating costs reduced by up to 70%.

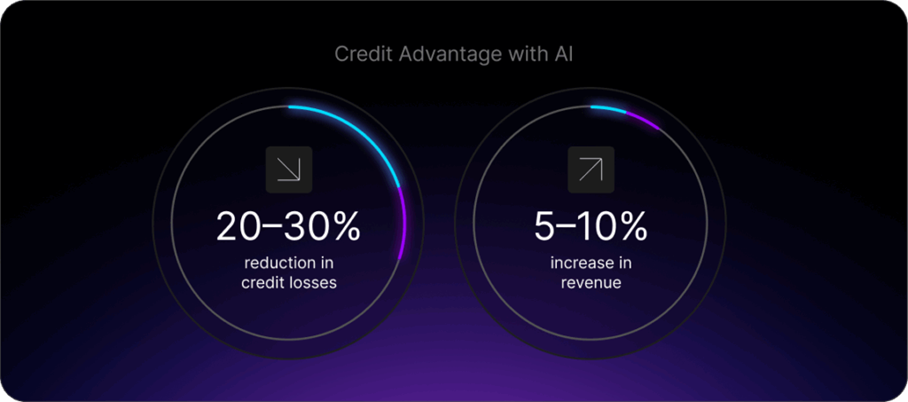

- Banks that fully integrate AI can reduce credit losses by 30% and increase revenue by 10%.

- Only 9% of firms consider themselves ahead of the curve, despite 90% having adopted AI.

Artificial intelligence has transformed the lending sector in recent years. The technology now powers predictive analytics that improve approval rates and reduce default risk. Natural language processing automates document reviews. Real-time transaction monitoring strengthens KYC and AML compliance. The results of AI’s impact on lending are clear: loan processing is up to 25 times faster, operational costs are reduced by 20%-70%, and fraud detection and credit risk accuracy are improved by over 80%, according to ScienceSoft Finance.

AI is no longer a differentiator in banking. It has become a baseline capability that customers expect. The question now is how banks can move beyond basic adoption to cutting-edge AI implementation. How can they gain a true competitive edge in lending?

Moving beyond basic AI implementation

Lenders need to advance past the initial stages of AI implementation to stand out, according to ScienceSoft. For customers, AI-powered lending delivers tangible benefits. These include faster approvals and more inclusive credit decisioning. Borrowers receive personalized offers and lower rates or fees. These improvements help banks meet customer expectations while building satisfaction, loyalty, and trust.

However, many banks struggle to transform early AI efforts into exceptional borrower experiences. A 2024 survey reveals a striking gap. While 90% of financial services firms have incorporated AI to some extent, only 9% consider themselves ahead of the curve, per a 2024 survey

Several factors explain this gap. legacy systems and data silos prevent banks from deploying fast-moving, innovative AI technologies. Much of the current AI adoption focuses on back-office functions. Customer-facing applications and strategic areas remain underutilized. Banks aiming to maximize AI potential must overcome these challenges quickly.

What next-generation AI lending looks like

It’s one thing to say that banks and lenders should adopt AI more rapidly, but what does that actually look like in practice?

Rather than thinking of the next generation of AI in lending through individual use cases, banks should approach it as a holistic overhaul, where AI tools are integrated into every step across the lending lifecycle, from initial application to servicing. Below are three key areas where AI is reshaping the future of lending for financial institutions.

Alternative data sources transform credit decisions

A mature, integrated AI stack enables lenders to move beyond traditional credit scoring. These systems analyze alternative data including bank transactions, spending patterns, and past activity. This comprehensive approach assesses creditworthiness more accurately.

The results are impressive, as research shows that banks fully integrating AI across the credit lifecycle achieve significant improvements. Credit losses drop by 20-30%. Revenue increases by 5-10%. This approach also expands credit access for borrowers who would be excluded under traditional credit scoring systems.

Ongoing risk assessment reduces defaults

Leading lenders now adopt AI-powered systems for continuous risk assessment. These systems dynamically adjust credit limits and interest rates based on real-time borrower behavior. Upstart, an AI lender in the US, exemplifies this approach. The company uses continuous AI-based risk assessment to adjust offers and pricing after origination. They report substantial reductions in default rates compared with traditional models.

For borrowers, real-time risk assessment brings practical benefits. Lenders can identify potential issues earlier. They can adjust repayment plans proactively, helping borrowers avoid default.

Customer engagement through personalization

By leveraging AI to examine customer behaviors in detail, banks and lenders can create hyper-personalized, tailored borrowing solutions, instead of one-size-fits-all products.

US FinTech SoFi, for instance, uses AI and machine learning (ML) technologies to personalize loan offers and financial advice based on the borrower’s current situation. For example, specific refinancing options for recent graduates with student loans.

The result is clear. Products and support align more closely with each customer’s unique financial situation and goals.

Major challenges in achieving advanced AI implementation

Becoming a market leader in AI-powered lending requires overcoming significant obstacles. Many lenders lack the technical foundations, cultural readiness, and regulatory expertise needed to advance their AI capabilities. To move from experimentation to transformation, banks must address several persistent barriers.

- Data quality and accessibility issues: Legacy systems create fundamental problems for AI implementation. Siloed data and inconsistent formats prevent AI models from accessing clean, real-time datasets. Only 26% of companies have developed the capabilities to move beyond proofs of concept. Even fewer generate tangible value from their AI initiatives.

- The AI skills gap: A significant skills gap exists between business stakeholders, data scientists, and IT teams. This disconnect slows deployment and prevents strategy alignment,third of banks report a shortage of AI skills. Nearly a quarter express hesitation about using AI tools due to lack of expertise.

- Navigating the regulatory landscape: These include the EU AI Act and DORA. Only 11% of FI firms feel prepared for upcoming AI regulations. Just 14% have implemented a fully functional AI ethics framework.

The path forward for lenders

Treating AI adoption as a future milestone is already outdated thinking. To lead, lenders must integrate AI into every stage of the lending lifecycle. This comprehensive approach spans from initial application through ongoing servicing.

Success requires dismantling data silos and modernizing core systems. Banks must build cross-disciplinary AI teams that can move as quickly as the technology evolves. They must navigate complex regulations while embedding AI ethics at the heart of their operations.

This transformation demands bold leadership and significant investment. However, the rewards justify the effort. Banks that succeed will create a lending model that operates faster and smarter. They will serve more customers inclusively while setting new standards for the AI era in banking.

For more expert content on industry outlooks and innovation, subscribe to our newsletter or visit our Insights page.

No, AI has become a baseline requirement rather than a competitive advantage. Banks without AI capabilities struggle to meet customer expectations for speed and personalization.