- Higher interest rates will increase the cost of borrowing for many consumers and businesses already under financial stress.

- Collections teams at smaller banks face the greatest pressure to manage higher volumes with reduced headcounts and legacy systems.

- AI-powered collections can significantly improve recovery rates, reduce operational costs, and increase customer satisfaction, research shows.

Collections teams at banks and financial institutions are facing higher delinquency rates following the outbreak of the Iran conflict, as energy prices surge, central bank policies tighten, and business and household finances weaken across major markets, reshaping the case for AI-powered collections. The US-Israel strikes on Iran, which began on February 28, have delivered a fresh shock to a global economy still recovering from high interest rates, sticky inflation, and the cost-of-living crisis in the wake of the Covid-19 pandemic. The conflict has generated a structural shock to the world economy, delivered at a moment of “geoeconomic fragility”, according to a report by the World Economic Forum.

“The war’s cascading economic fallout is now radiating well beyond the Gulf, reshaping global commodity markets, food systems, industrial supply chains, financial conditions, and geopolitical alignments – potentially for years to come,” the WEF notes.

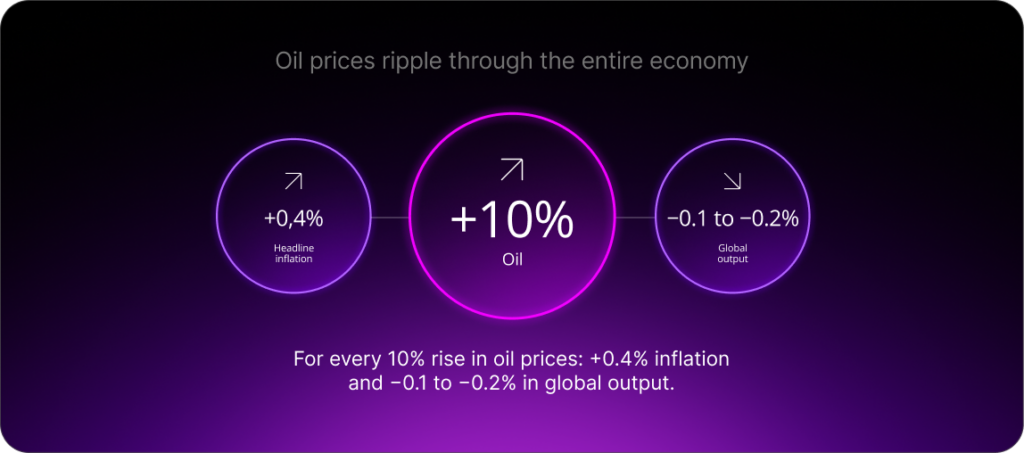

Meanwhile, the International Monetary Fund estimates that for every 10% rise in oil prices, there is a 0.4% increase in headline inflation and a 0.1% to 0.2% drop in global output. The response from central banks, many of which met in the week of March 16-19, highlights the seriousness of the outlook, with the US Federal Reserve holding its benchmark rate at 3.5% to 3.75% and revising its inflation forecast upward to 2.7%.

The European Central Bank also held its rate at 2%, saying the war in the Middle East has made the outlook “significantly more uncertain, creating upside risks for inflation and downside risks for economic growth.” In contrast, the Reserve Bank of Australia hiked its rate by 25 basis points to 4.1% – a 10-month high – citing inflationary concerns and the conflict in the Middle East. For the collections sector, the implications are clear: higher or sustained interest rates will increase the cost of borrowing for many consumers and businesses already under financial stress.

Even before the Iran conflict, delinquency rates on loans were on the rise globally. In the US, for example, data from the Federal Reserve Bank of New York’s Quarterly Report on Household Debt and Credit shows that delinquency rates rose to 4.8% of all outstanding household debt in the fourth quarter of 2025.

It is a similar scenario for businesses in the EU, where bankruptcies rose by 2.5% in the fourth quarter of 2025, according to Eurostat data. In France alone, business insolvency rates rose to pre-Covid record levels in the first eight months of 2025, according to a payment survey by Coface. And in the UK, company insolvencies reached 1,878 in February, up 7% from January, government data shows. The issue for collections teams is no longer just about rising volumes, it is whether they have the tools to manage the increase while preserving customer relationships, particularly for smaller tier 2 to tier 4 banks, which are facing increased pressure as they cope with reduced headcounts and rely on legacy systems to manually process cases.

The case for AI-powered collections

Against this backdrop, the automation of collection processes has never been more urgent. The global debt collection software market was valued at $4.8 billion in 2025 and is expected to reach $11.3 billion by 2034, reflecting a compound annual growth rate of 8.89%, according to a report by the IMARC Group.

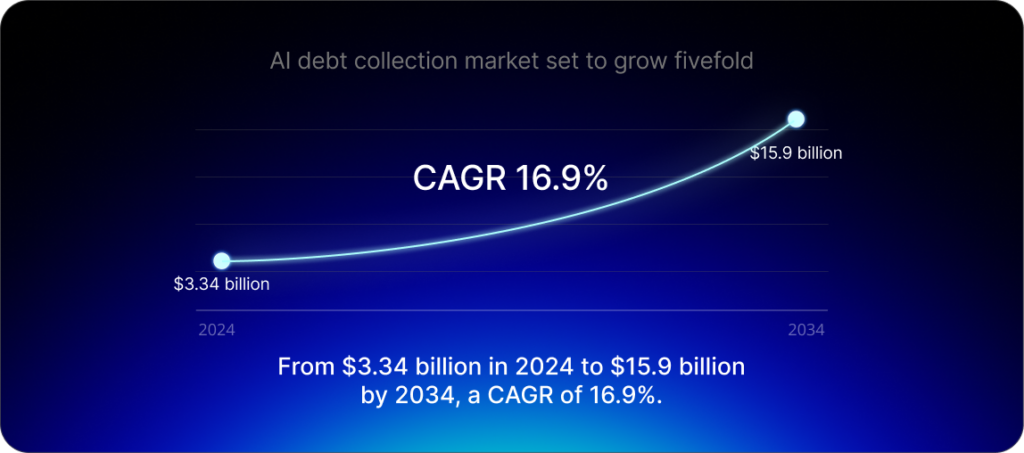

However, it is the global AI for debt collection segment that is expected to boom over the next decade as banks increasingly recognise the advantages of automation. The market is expected to grow at a CAGR of 16.9%, from $3.34 billion in 2024 to $15.9 billion in 2034, research by market.us shows.

Advanced generative AI capabilities in customer assistance and collections can boost recovery rates by about 10%, lower operational costs by up to 40%, and increase customer satisfaction levels by as much as 30%, according to research by McKinsey.

Why empathy matters in modern debt recovery

Recent research by KPMG shows that the banking sector’s overall customer experience score improved in 2025, with the empathy pillar rising by 1.4%, suggesting that customers felt a stronger emotional connection with their banks.

“The expectations pillar also improved, rising by 1.3% and indicating progress in how effectively banks are meeting customer needs,” KPMG notes in the report.

When banks use AI-powered digital communication, such as apps, messages, and portals, to show an understanding of individual situations and offer clearer, easier repayment options, customers perceive more empathy and better expectation-setting – conditions that support higher repayment and resolution rates.

By automating collection processes, customers can access self-service features, such as payment plans and restructuring options, without agent intervention. This means that collection teams can focus on high-value cases and have more time to support financially fragile customers. The automation of collections is not just a cost-reduction exercise – it is a performance lever. Each debtor’s profile responds differently, and a modern collection solution must orchestrate the right communication channel at the right moment.

Building an AI-powered collections team

Digital transformation is not without its challenges; for example, legacy systems will have to be updated, staff retrained, and manual workflows reorganized. Regulatory requirements will also need to be considered, such as the EU’s General Data Protection Regulation and consumer protection laws in individual countries. This will create further requirements around governance, traceability, and human oversight, particularly for fragile customers.

However, for banks and financial institutions that have yet to develop AI-powered collections capabilities, the urgency is intensifying as teams face increasing pressure amid a weakening global economic outlook.

Banks that enable automation and intelligent segmentation through machine learning, along with personalized customer follow-up, will help collection teams manage crisis-driven volume increases without the need to increase headcounts. This will result in a more efficient and empathetic collections process that frees up agents to focus on areas where human judgment matters most.

Get in contact with a member of our team today.

Q&A: Five Questions on AI and automation in collections

The Iran conflict is the latest shock to a global economy that was still recovering from high interest rates, sticky inflation, and the cost-of-living crisis following the Covid-19 pandemic. Rising energy prices are putting pressure on household and business finances, while central banks are warning of risks to inflation and the possibility of higher interest rates amid slowing economic growth.