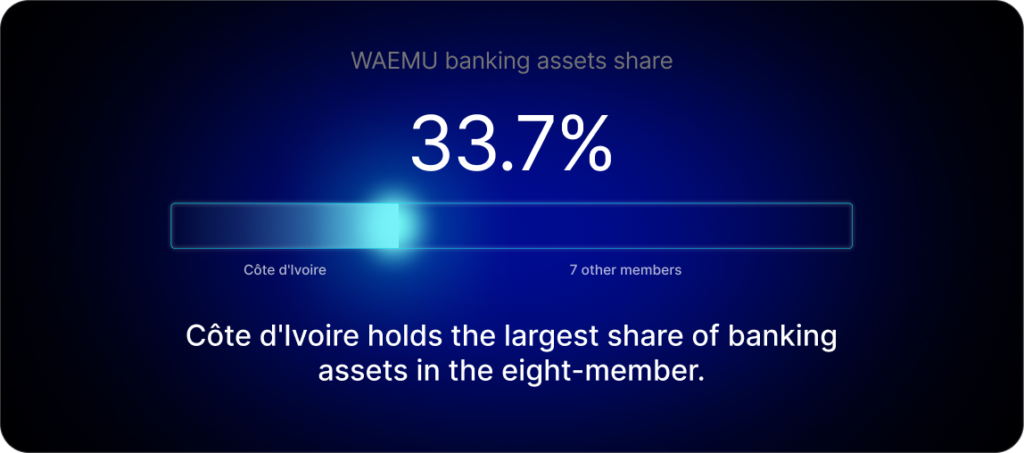

- Côte d’Ivoire holds 33.7% of all banking assets in the WAEMU, the largest share among its eight member states.

- Financial inclusion in Côte d’Ivoire has risen from 41% in 2017 to 51% in 2025, driven primarily by mobile money adoption and microfinance expansion.

- The country has over 28 million registered mobile-money accounts and 13 million active users.

Côte d’Ivoire has emerged as the banking and financial services hub of West Africa, driven by a hybrid model of traditional banking services, mobile money, and fintech platforms. Today, the country holds a third of all banking assets in the West African Economic and Monetary Union (WAEMU), accounting for the largest share among the eight-member bloc at 33.7%, according to government data. However, to maintain this regional dominance and the share of the industry that traditional banks maintain, investment in digital is needed.

The capital of Abidjan is at the heart of the country’s financial system, playing host to numerous bank headquarters and West Africa’s Bourse Régionale des Valeurs Mobilières (BRVM) stock exchange, as well as a rapidly expanding fintech ecosystem. The government data also shows that the total balance sheet of credit institutions amounts to 22.19 trillion West African CFA francs (US$40.19 billion), while 32 licensed banks and financial institutions are based in the capital. Of those, 28 are banks, 15 international and 13 sub-regional, and the remainder are financial institutions with banking characteristics, the data shows.

Meanwhile, the top five banks in Côte d’Ivoire in 2024 are:

| Bank | Assets (FCFA / US dollar) |

| Société Générale Côte d’Ivoire | 3.6 trillion / 6.48billion |

| NSIA Banque | 2.5 trillion / 4.50 billion |

| Banque Nationale d’Investissement | 2.3 trillion / 4.14 billion |

| Banque Atlantique Côte d’Ivoire | 2.29 trillion / 4.12 billion |

| Ecobank Côte d’Ivoire | 2 trillion / 3.6 billion |

| Source: In Côte d’Ivoire |

Traditional banks remain central to the stability of Côte d’Ivoire’s financial system. To maintain their strong position, they are increasingly investing in modernizing their core systems. We are seeing this with many SBS clients that are eager to upgrade to the latest version of SBS Core Amplitude, in order to take advantage of new digital capabilities.

In our Banking is Local series, we explore the rise of Côte d’Ivoire’s financial sector as it continues to focus on financial inclusion, digital innovation, and regional integration.

Historical roots: Abidjan and the Côte d’Ivoire banking sector

Abidjan’s journey as the financial hub of West Africa has been decades in the making, beginning with the launch of the African Development Bank in the city in 1965.

While the banking sector was tested by commodity price collapses and a brief civil conflict in the 1980s and 1990s, it emerged more resilient in the following decades. Economic recovery, regulatory reform, and renewed foreign investment in the 2010s helped reposition Abidjan as the financial center of WAEMU, resulting in a range of regional and international banks setting up their headquarters in the city.

Of the 21 institutions in WAEMU with total assets exceeding 1 trillion FCFA (about US$1.8 billion), 11 operate in Abidjan, according to the government. This represents a staggering 52% of the major regional banks and 40% of the 28 institutions present in Côte d’Ivoire’s market, reflecting the “economic weight and depth of the national financial system,” it adds.

From informal savings to mobile money infrastructure

Despite the scale of the country’s formal banking sector, millions of people remain underbanked or unbanked in Côte d’Ivoire. However, financial inclusion has grown from 41% in 2017 to 51%, according to government statistics based on the 2025 World Bank’s Global Findex survey.

“This improvement is linked to the development of mobile money, the promotion of microfinance institutions and government actions,” it says.

Meanwhile, an estimated 80% of household savings in 2020 were held outside of traditional banks, reflecting the continued importance of cash, community savings groups, and informal financial arrangements.This shift has led the country’s financial system to move toward accommodating citizens who lack formal bank accounts but hold informal savings. For example, a state-guaranteed national savings scheme launched through the Caisse des Dépôts et Consignations (CDC-CI) aims to move informal savings into the formal system.

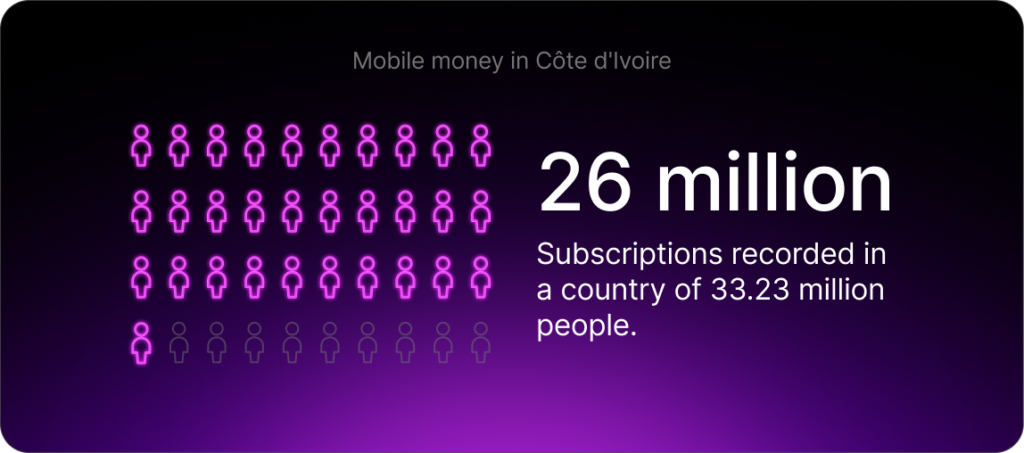

Mobile money services have played a central role in this transition. What began as a financial inclusion tool has evolved into a payment system that allows peer-to-peer transfers and merchant and bill payments, among other services. With a population of about 33.23 million, a report by Socialnetlink estimates that 70% of adults use at least one mobile money service. This is reflected in data published in the 2024 annual report by ARTCI, Côte d’Ivoire’s telecoms regulator, which reported that there were more than 26 million mobile money subscriptions as of December 31, 2024.

Leading mobile providers include telecom-backed platforms and fintechs. According to ARTCI, Orange Money is the largest platform, with more than 13.83 million subscriptions. This is followed by MTN Mobile Money (MoMo) with more than 8.46 million subscriptions, while Moov Money is the country’s third-largest platform with over 2.87 million subscriptions. However, ARTCI does distinguish between registered or active accounts in its report.

Wave, a fintech company from Senegal, has expanded into Côte d’Ivoire with its mobile money service and has also launched a licensed commercial bank, Wave Bank Africa.

Fintechs are flourishing in the financial system

The rapidly expanding fintech sector is also addressing gaps in consumer and business banking. This includes the Abidjan-based Djamo, which has positioned itself as a neobank that offers affordable accounts, payments, and financial tools to the country’s underbanked population. Since its launch in 2020, it has grown its customer base to over one million, including 10,000 small and medium-sized enterprises.

Another local fintech, Julaya, focuses on business payments and cash management. Founded in 2018, the company provides business-to-business digital accounts layered on mobile money rails.

Interoperability: Progress driven by regulation

Regulation is also playing a decisive, albeit uneven, role in shaping the financial ecosystem, particularly when it comes to interoperability. In 2022, the Central Bank of West African States (BCEAO) approved a framework that enabled mobile money platforms to interconnect, allowing users to transfer funds across services seamlessly. The country has also adopted the GIM-UEMOA interbank card system.

WAEMU’s Interoperable Instant Payment Platform was also launched regionally to facilitate real-time payments across member states. Adoption remains limited, but it highlights a regulatory push toward greater integration across banks, mobile money services, and fintechs.

Core banking modernization in the Côte d’Ivoire banking sector

Upgrading legacy core systems has become a priority for many banks in Côte d’Ivoire, a necessary move to support real-time payments, streamline operations, and provide a stable foundation for modern digital banking platforms that connect banks with mobile money ecosystems and fintech partners. For example, in 2025 BMS Côte d’Ivoire selected SBS to upgrade its core banking system, not only nationally, but across the West African sub-region, with the latest version of SBS Core Amplitude to streamline operations and improve performance.

BMS now benefits from the latest functional and technological enhancements of SBS Core Amplitude, ensuring continuous improvement and future readiness to meet the evolving needs of the bank’s customers in a fast-changing financial landscape.

As Côte d’Ivoire continues on its journey as West Africa’s financial hub, the country’s financial system has also emerged as a regional benchmark. By combining traditional banking with mobile money adoption and fintech innovation, it is designed to handle local realities like how people save, pay, and do business, rather than relying on imported models.

For more expert content on industry outlooks and innovation, subscribe to our newsletter or visit our Insights page.

Questions and Answers

Government data shows that the country holds 33.7% of all banking assets in the West African Economic and Monetary Union (WAEMU), accounting for the largest share among the eight-member bloc.