At its heart, banking has always been about relationships. Yet in today’s digital world those relationships are increasingly defined by how well an institution can make each customer feel recognized as an individual. The days of one-size-fits-all services are fading fast. Banking personalization now defines this shift, customers now expect the bank in their pocket to know as much about their needs as the branch manager once did. The rewards for meeting this expectation are clear. A customer who feels understood is far more likely to remain loyal. Research by EY suggests that 40% of customers would be more inclined to stay with a financial services provider if it offered more personalized service. In practice, this can be as simple as a savings prompt when someone’s salary lands, or as sophisticated as anticipating when a young family may be ready for a mortgage.

Digital convenience is central to this shift. For many, banking through a mobile app is no longer a nice-to-have but a basic requirement. Surveys show that more than seven in ten adults in Australia believe they should be able to complete any financial task from their phone, with customers in the UK and US not far behind. The message is consistent: convenience, powered by personalization, is now the benchmark.

And it is not only customers who benefit. Banks that invest in centralized analytics and streamlined processes see clear benefits, generating 5–15 % more revenue from campaigns and launching them two to four times faster than less data‑savvy competitors. For boards and balance sheets, personalization is not only a matter of customer satisfaction. It is a strategic imperative.

The trust problem for data-driven personalization

There is a paradox at the heart of personalization. While on the one hand it offers banks a powerful opportunity to strengthen their relationships with customers, on the other it requires access to sensitive personal data, an area where trust can be fragile and easily eroded. Every personalized recommendation, alert or product offer depends on data, such as what customers spend, save and borrow. If customers begin to feel that this information is being used in ways they don’t understand, or for the bank’s benefit rather than their own, trust can quickly unravel.

The stakes are especially high in banking, where trust has long been the strongest differentiator for traditional players. A survey by Accenture found that 81% of customers across 17 countries trust their primary bank to keep their data secure. That figure drops to 58% for other traditional banks and just 45% for digital-only challengers. Banks that have earned decades of customer confidence therefore stand to lose the most if that trust is compromised.

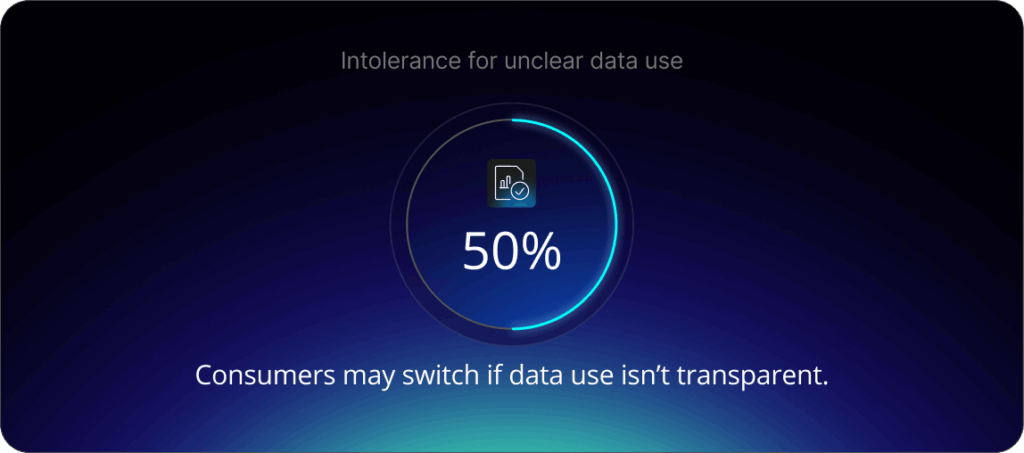

Consumers are also more unforgiving than ever. Nearly half say they would consider switching providers if they are not given clear explanations about how their data is used. The consequences of failure can be swift and punishing. When Capital One suffered a breach in 2019 that exposed the personal information of more than 100 million customers, its stock fell nearly 6% within days. The company was fined $80 million by regulators and ultimately paid out more than $190 million in customer settlements. For a bank that had positioned itself as tech-forward, the reputational damage was profound, serving as a warning that in the digital age, a single lapse in data protection can undo years of careful brand-building.

Why transparency and regulation matter for personalization in banking

If data is the engine of personalization, then transparency is the oil that keeps it running smoothly. Customers will only consent to sharing information if they believe it is being handled responsibly and for their benefit. That means banks must do more than meet legal obligations; they need to communicate openly about how data is collected, stored and used. In practice, this could be as straightforward as privacy notices written in plain language, opt-in and opt-out choices that are genuinely simple, or dashboards that show customers how their data shapes the services they receive.

Artificial intelligence is what makes personalization possible at scale. It allows banks to move beyond generic offers and instead anticipate individual needs in real time, whether by flagging unusual spending, recommending savings products or tailoring credit decisions. Yet the same technology can also raise suspicion. Algorithms may be able to spot patterns invisible to the human eye, but their recommendations risk looking opaque or arbitrary. Explainable AI, systems where decisions can be interpreted and justified, is therefore becoming essential. Customers are more likely to trust a personalized loan offer or fraud alert if they can see why it was generated, rather than assuming it came from a “black box” they don’t understand.

Here, regulators are not merely obstacles but vital allies. Frameworks such as GDPR in Europe, Open Banking initiatives in markets like the UK and Australia, and the UK’s new Consumer Duty rules provide the guardrails that ensure innovation is safe, ethical and fair. Compliance with these rules is not only about avoiding penalties; it is a visible signal to customers that their bank takes privacy and fairness seriously.

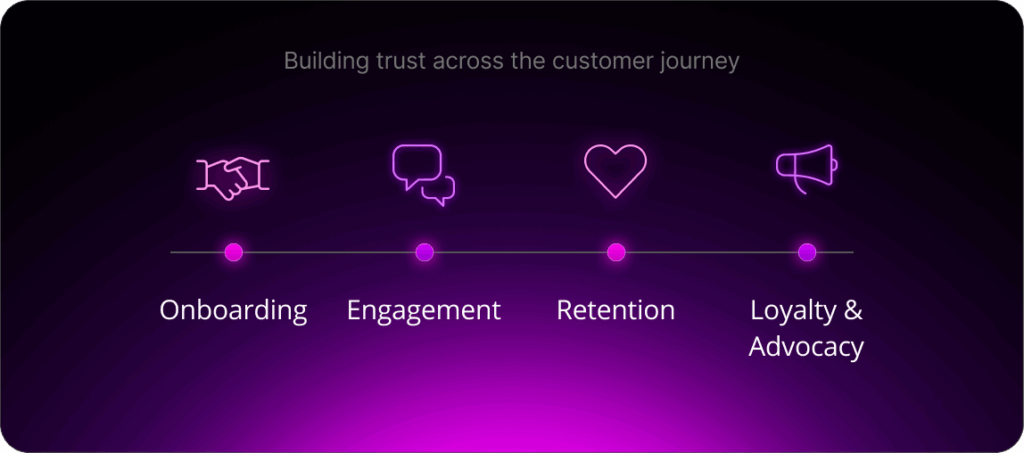

Building trust into every stage of the journey

For banking leaders, the challenge is not only to embrace personalization but to embed it responsibly at every stage of the customer relationship. Done well, data-driven personalization can build trust rather than undermine it. The key is to design each touchpoint so that customers see clear value in sharing their data, and understand how it is being used.

Onboarding

The first interaction sets the tone. Data can remove friction by pre-filling forms or guiding customers toward products suited to their profile. At the same time, banks must be upfront about what information is being collected and why. Transparency at the start builds confidence that will carry into the relationship.

Engagement

Day-to-day banking offers the richest opportunities to demonstrate the benefits of personalization. Proactive insights, timely fraud alerts and contextual product recommendations can feel supportive rather than intrusive if they are easy to understand and clearly linked to customer needs. Reliability and clarity matter more than volume of interactions.

Retention

As customers move through life stages, their financial needs change. Personalization allows banks to anticipate these moments, whether it is offering a mortgage to a growing family or retirement planning to a mid-career professional. The risk is that personalization slips into overreach, which can erode trust. The safeguard is to frame every recommendation as a service to the customer, not as a sales tactic.

Loyalty and advocacy

Long-term relationships depend on more than transactions. Banks can reinforce loyalty by offering tools for financial wellness, recognizing milestones such as anniversaries or savings achievements, and providing tailored wealth planning. Each of these actions should rest on secure data practices and a commitment to ethical AI. Customers who feel respected in this way are more likely to become advocates, recommending their bank to friends and family.

Personalization is not a one-off initiative. It is a discipline that must be integrated throughout the customer journey, balancing insight with integrity. Banks that commit to this balance can use data not only to deepen engagement but to strengthen the trust that underpins every successful banking relationship.

Personalization in banking, driven by customer trust

Personalization has become the defining frontier in modern banking. Customers want their financial institutions to recognize them as individuals, anticipate their needs and deliver services that fit seamlessly into their lives. The commercial case is equally strong: banks that embrace data-driven personalization see faster growth and stronger customer loyalty.

But personalization cannot succeed without trust. Data is the foundation of tailored services, and customers will not share it freely if they fear it is being misused.

The question, then, is not whether to personalize but how to do so responsibly. Executives should ask themselves: Are our personalization initiatives building confidence or eroding it? Are we clear about how data is collected and applied? Are our AI-driven decisions explainable and fair?

The path forward is practical. Audit data practices and customer communications. Ensure analytics are transparent and aligned with ethical standards. Treat regulation as a framework that enables innovation safely. Above all, remember that personalization and trust are not competing priorities. They are complementary forces that, when managed together, can deepen relationships and unlock sustainable growth. Banks that can strike this balance will not only keep pace with customer expectations. They will lead the industry into a future where being personal also means being trusted.

For more expert content on industry outlooks and innovation, subscribe to our newsletter or visit our Insights page.

Watch Andrew Steadman share his perspective on this topic at the 2025 Summit.