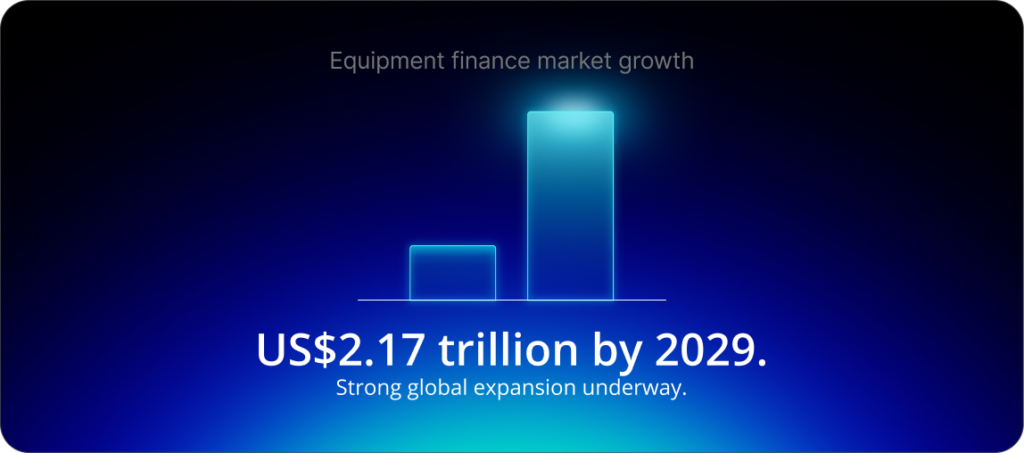

- The equipment finance service market is expected to grow from US$1.30 trillion in 2024 to US$2.17 trillion by 2029.

- Automotive finance market reached the mid-US$300 billion range and is projected to grow at roughly 7% annually through 2030.

-

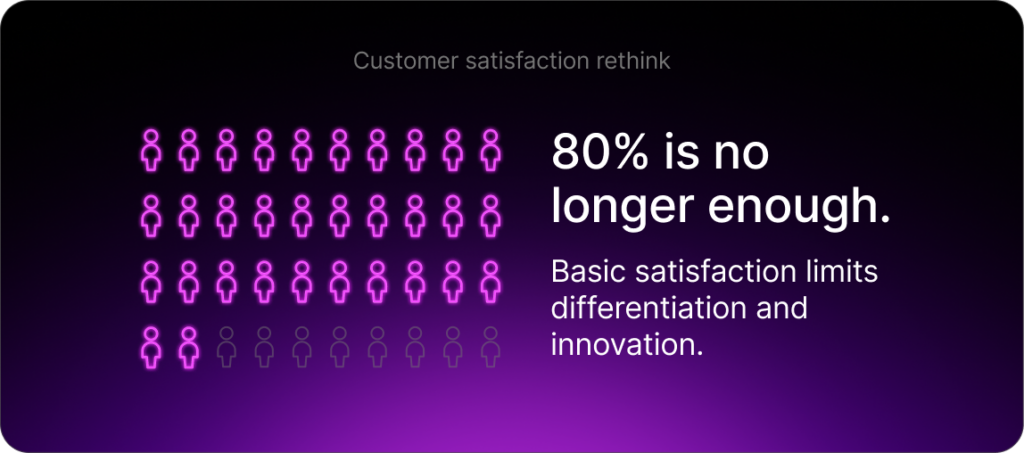

80% customer satisfaction is no longer “good enough,” as digital-first experiences mean basic expectations limit differentiation and stifle innovation.

Globally, automotive and equipment finance markets continued their upward trajectory in 2025, supported by strong demand for new vehicles, capital equipment and flexible financing solutions. This momentum now shapes asset finance in 2026, with recent forecasts placed the equipment finance service market at approximately $1.45 trillion, rising from about $1.30 trillion in 2024, with growth expected to continue toward $2.17 trillion by 2029. And automotive finance followed a similar path, with the market reaching the mid-$300 billion range and projected to grow at roughly 7% annually through 2030.

While the numbers are encouraging, 2025 made clear that growth alone isn’t enough. The asset finance sector is shifting rapidly, shaped by technological change, evolving customer expectations and new regulatory pressures. Many of these were highlighted in the SBS study published at the beginning of the year, Asset finance in 2025: Trends and Innovations, where we also discussed the need for organisations to embrace innovation and reduce reliance on legacy processes. To understand how the industry is continuing to evolve, it is vital to look at how predictions from 2024 compared to the realities of 2025, and how we can use these learnings to look forward to 2026 and beyond.

| Theme | 2024 Expectation | 2025 Reality |

| Real-time data | Align sources; reduce error and latency | Embedded decision engines; faster onboarding; predictive fraud detection |

| Customer experience | Digital channels will grow | CX became a core differentiator; service expectations rose sharply |

| Auditing | Digital audits will expand | Hybrid models matured; higher frequency at lower cost |

| AI in finance | Early adoption period | Operational AI emerged; governance and compliance scrutiny increased |

Real-time data and dynamic decisioning

At the start of 2025, it was clear that real-time data was becoming a cornerstone of dynamic pricing and faster credit decisioning. Organisations that prioritised accurate, integrated data were better positioned to make informed business decisions and identify potentially fraudulent activity at an earlier stage. As onboarding processes accelerated through the use of real-time data, speed quickly emerged as a competitive differentiator. Faster, more consistent decisioning supported higher conversion rates, improved customer satisfaction and increased confidence across dealer networks.

At the same time, the role of decisioning models evolved. Instead of relying on legacy scorecards applied late in the application process, lenders increasingly embedded dynamic risk and pricing engines directly into digital journeys. By integrating decision models earlier, organisations were able to deliver near-instant outcomes while maintaining strong risk controls.

This shift matters. Instant and near-instant decisions are no longer simply an operational improvement, they directly influence customer experience, dealer trust and overall competitiveness. Those that delayed investment in real-time data capabilities during 2025 often found themselves constrained by manual bottlenecks, longer cycle times and slower responses to emerging risk signals.

Why is “good enough” customer experience no longer enough?

Customer experience took on renewed importance in 2025. Previous research has consistently shown that a significant proportion of consumers are willing to pay more for quality service, but this year reinforced a broader truth: buy-in from dealership staff is just as critical as satisfaction at the end-customer level. Positive dealer colleague engagement supports smoother operations and faster processing times, delivering benefits across the business and creating a knock-on effect for retail customers.

One theme that became increasingly clear throughout the year was that the long-standing benchmark of 80% customer satisfaction is no longer considered “good enough.” As digital-first experiences become the norm, focusing only on meeting basic expectations risks limiting differentiation and stifling innovation. Leading organisations began looking beyond traditional satisfaction metrics, placing greater emphasis on ease of use, speed and consistency across every interaction.

To support this shift, lenders continued to invest in more efficient servicing processes through digital dashboards, mobile applications and self-service portals. Rather than introducing disconnected tools, the focus was on embedding meaningful actions directly into existing digital workflows. This approach enabled dealers to manage financing activities more effectively, strengthening dealership loyalty and, in turn, customer loyalty.

As expectations around self-service continue to rise, organisations increasingly began to review which processes could be simplified or adapted for mobile use. Enabling dealers to service assets seamlessly, from the auction room through to the asset leaving the lot, became an important factor in delivering a modern, friction-free experience for all parties involved.

How are lenders rethinking auditing and risk management?

Digital auditing continued its rapid rise in 2025, building on the momentum established during the COVID-19 pandemic. What began as a practical response to lockdowns and travel restrictions has proven to be a durable and scalable approach to managing inventory risk across auto and equipment finance portfolios.

Over the past 12 months, this shift was demonstrated at scale when a major independent inventory finance company implemented the SFP Digital Audit solution across 18,000 US auto dealerships, completing more than 100,000 audits through the platform. This level of coverage highlighted how digital auditing can support consistent, frequent oversight in ways that traditional physical audits alone cannot.

While advances in artificial intelligence and machine learning continue to strengthen digital auditing capabilities, the value of human expertise remains critical. As a result, many lenders increasingly adopted hybrid auditing models, combining continuous digital monitoring with targeted physical inspections to manage risk in near real time. This approach balances efficiency with oversight, ensuring complex or higher-risk scenarios still benefit from human judgement.

Both digital and hybrid auditing models place governance at the centre of wholesale operations. By enabling earlier risk identification and more consistent controls, they support compliance with evolving regulatory requirements while helping organisations maintain confidence in the integrity of their floorplan portfolios.

AI and compliance in asset finance

AI continued its transition from an emerging technology to an operational capability in 2025, with lenders increasingly applying AI to accelerate onboarding, strengthen fraud detection, and personalise communications with both dealers and customers. Generative AI also expanded its role, creating new opportunities to streamline internal workflows and deliver tailored insights at scale. For asset finance, the benefits of AI extend beyond faster processing and operational efficiency. Used effectively, AI improves early-stage risk detection, enabling organisations to identify anomalies and potential fraud sooner, while also supporting hyper-personalised experiences that strengthen satisfaction and retention.

At the same time, compliance expectations grew more complex in 2025. Regulators placed heightened scrutiny on fairness, explainability and data governance, as AI-driven decisioning became more widespread. Frameworks such as Europe’s Digital Operational Resilience Act (DORA) further emphasised the importance of operational controls, resilience testing and transparent oversight of technology-enabled processes. As a result, many organisations spent 2025 balancing acceleration with governance, expanding AI use cases while ensuring models remained auditable, bias-tested and aligned with internal policies.

Asset finance in 2026 and beyond

As the industry looks ahead to 2026, asset finance organisations are preparing for another year of continued transformation. While 2025 presented its share of challenges, it also reinforced the role of innovation as a driver of resilience and growth. Several themes are already emerging as priorities for the year ahead:

- Deeper floorplan digitisation, extending beyond auditing into broader lifecycle automation

- Continued growth in cybersecurity requirements, particularly for cloud-native and integrated ecosystems

- Further integration of data and AI across servicing, pricing and operations, supported by stronger governance frameworks

- Greater emphasis on partnerships, as organisations seek expertise across technology, regulation and operational change

The combination of data, AI and hyper-personalisation is expected to be a powerful force, but regulatory and compliance demands will continue to raise the bar, particularly as cyber risk remains a top concern globally. Navigating this environment will require careful balance: accelerating innovation while maintaining control, transparency and resilience.

In 2026, asset finance businesses face challenges that differ from the wider financial services market, including the need to manage physical assets, complex dealer networks, and regulatory variation across regions. As SBS prepares to launch its latest Asset Finance Trends study for 2026, one thing is clear: organisations that succeed will be those that modernise intelligently, supported by partners who understand the unique demands of the asset finance ecosystem.

In 2024 alone, SBS supported more than 30,000 dealerships across multiple industry leaders, helping to process 4.6 million units globally. This experience continues to inform how SBS partners with asset finance organisations as they prepare for the opportunities and challenges that lie ahead. Find out how SBS can support your asset finance strategy as the industry continues to evolve. Get in contact with a member of our team today.

Questions and Answers

The global equipment-finance services market is estimated to be worth approximately $1.45 trillion in 2025, continuing a strong growth trajectory toward more than $2 trillion by the end of the decade.