- Since the 1997 Asian financial crisis, the government has transformed the country into a broadband nation, paving the way for its open banking system.

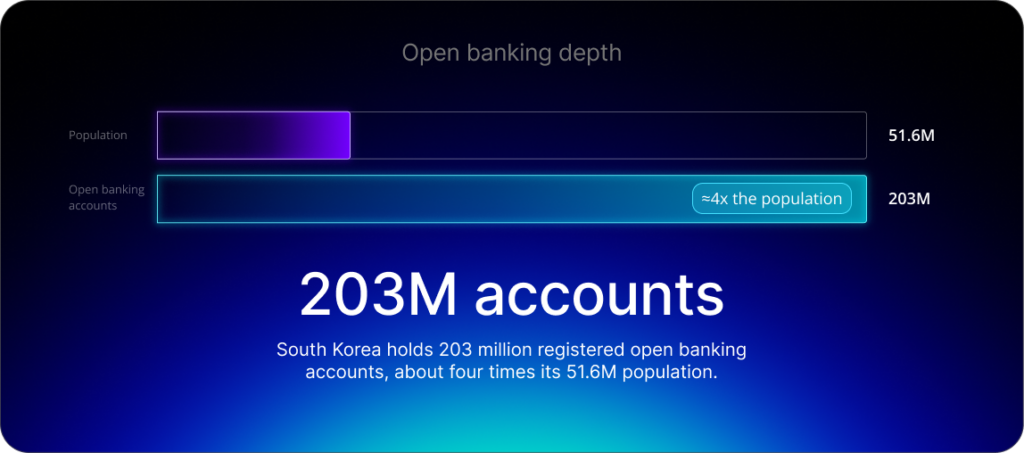

- With a population of 51.6 million, South Korea boasts 203 million registered open banking accounts.

- The most-used banking super-apps include Toss and KakaoBank.

South Korea’s open banking transformation has been years in the making, driven by a super-app ecosystem built on trust. In comparison, France’s open banking experiment remains modest despite the introduction of the European Union’s revised Payment Services Directive (PSD2) in September 2019, which aims to improve the security of payment transactions and protect consumer data. However, a Mastercard survey found that just 4% of French consumers are familiar with open banking, while adoption is at 8.5%. A recent Sopra Steria study also found that 62% of French consumers refuse to share their banking data without stronger guarantees.

A similar data-sharing framework covers 203 million registered open banking accounts in South Korea – a figure that far exceeds the country’s population of 51.6 million, reflecting the depth of multi-account usage among consumers. The difference in data-sharing between France and South Korea is not regulatory. Rather, it is cultural, historical, and structural and it begins with the 1997 Asian financial crisis.

In our Banking is Local series, we explore South Korea’s financial system, a market shaped by crisis, rebuilt on broadband access, and now running on super-apps, such as KakaoBank and Toss, that double as banks.

How the 1997 crisis built South Korea’s banking foundation

Understanding today’s open banking landscape in South Korea is not possible without the context of the Asian financial crisis, which began in Thailand in July 1997 and quickly spread throughout the region.

Before the crash, lending decisions in South Korea were based on collateral rather than risk analysis, while there was a belief that major institutions could not fail, according to a report by the IMF. The average debt-to-equity ratio in the manufacturing sector had reached nearly 400%, almost double the OECD average, and the top 30 chaebols – South Korea’s large family-owned conglomerates – exceeded 500%, the IMF added. On November 21, 1997, South Korea formally requested IMF assistance. The bailout totaled $58.5 billion, the largest in IMF history at the time, while unemployment had jumped from 2.6% to 8.7% by February 1999.

However, the government’s response to the crisis was a strategic bet: make South Korea the world’s first broadband nation. Under the Cyber Korea 21 program, the government invested $620 million to establish high-speed networks in dozens of major cities across the country. By 2001, broadband had reached 50% of Korean households and 30% of the population had registered for internet banking, while more than 70% of South Koreans had broadband access by 2004.

This infrastructure, built as a direct response to the 1997 financial crisis, has served as the foundation for the country’s widely used super-app ecosystem, including KakaoBank and Toss.

South Korea’s banking market today

South Korea’s banking sector is dominated by four major banks, all headquartered in Seoul:

| Bank | Total assets USD (2023) |

| KB Kookmin Bank | $409.07 billion |

| Shinhan Bank | $392.46 billion |

| Hana Bank | $385.01 billion |

| Woori Bank | $337.04 billion |

Source: ADV Ratings

The Bank of Korea sets monetary policy through a base rate, equivalent to the ECB’s deposit rate in Europe. The rate currently stands at 2.5%, unchanged since July 2025.

One distinct financial product that has emerged in South Korea is Jeonse, which has no direct equivalent elsewhere in the world. The informal lending practice began several hundred years ago but rose in popularity in the 1960s and 1970s, when rural workers moved to cities during the country’s transformation as an industrialized economy and needed housing.

Jeonse is a leasing arrangement that requires tenants to pay large upfront deposits, usually 50% to 80% of a property’s value. No monthly rent is required and the deposit is returned in full at the end of a lease. It allows renters to reduce their housing expenses and accumulate savings, putting them on a path to homeownership. At the same time, landlords can use the deposit as capital for other real estate investments. Jeonse emerged when South Korea’s formal lending system was still maturing, functioning as a market-driven answer to a banking gap, and it remains deeply embedded in the country’s housing and financial culture.

The rise of mobile banking

According to Statista, 79% of South Korean consumers use mobile banking, one of the highest penetration rates in the world. At the end of 2024, mobile banking subscribers had reached 203.6 million accounts, up 9.2% year over year, data from the Bank of Korea’s Payment and Settlement Systems Report 2024 shows.

As of March 2025, the most-used banking app in South Korea was Toss, with 24.08 million users, followed by KakaoBank with 18.35 million, according to Statista.

However, South Korea’s mobile payment ecosystem has a wider reach, with the likes of Naver Pay, KakaoPay, and Toss Pay accounting for a combined 81.5 million monthly active users. In 2024, fintechs offering mobile payment services accounted for 70.3% of the total mobile payments market.

KakaoBank and Toss: Two super-apps

South Korea’s super-app banking ecosystem is dominated by two players built from opposing starting points. With 49.1 million monthly active users as of the first quarter of 2025, effectively the entire adult population, KakaoTalk is the primary communication platform in South Korea. When the company launched KakaoBank in July 2017, it was pinning its success on an existing relationship rather than pitching to a new market.

The result: 300,000 customers in 24 hours, 2 million within a fortnight, and ₩1 trillion in savings in the first weeks. According to KakaoBank’s fourth quarter 2024 earnings report, the app had 24.88 million customers, an operating profit of ₩606.9 billion, up 27% year-on-year, and total assets of ₩62.8 trillion. Penetration is highest among Koreans in their 30s (84%) and 20s (81%), but it is expanding steadily across all age groups. The 50s age group, for example, has reached 52%, up from 44% in 2023. KakaoBank has since expanded in Asia, with SuperBank Indonesia attracting more than 5 million customers and a joint venture signed with Thailand’s SCBX in January 2025.

On the other hand, Toss was developed out of frustration. In 2014, a simple money transfer in South Korea required a government-issued digital certificate, a dedicated security plug-in, and multiple authentication steps – all in Internet Explorer. Toss replaced that process with a single tap. In July 2025, Toss had 30 million users, about 60% of the population, including 95% of Koreans in their 20s and 87% in their 30s. According to the company’s 2024 full-year results, Toss posted consolidated revenue of ₩1.95 trillion, up 42.7% year over year.

Open banking and MyData: South Korea’s regulatory framework

A number of policy initiatives have shaped South Korea’s open banking system, including the 2016 launch of a joint open platform by the Korea Financial Telecommunications and Clearings Institute, which covered account information inquiry and fund transfers across 16 banks. This formal open banking system was launched for commercial banks in December 2019.

However, it was the reciprocity principle, introduced in 2020, that was a game-changer for the industry. This mandated that fintechs had to share data in return, rather than just accessing it, and transformed the system from a one-way API into a data-exchange ecosystem.

This paved the way for the launch of MyData in 2022. According to the country’s Financial Services Commission, MyData is a world-first service that guarantees the data privacy rights of individuals. It enables users to aggregate financial data from banks, fintechs, insurance companies, and credit providers into a single app. As of April 2024, 69 licensed providers had been approved to offer MyData services, while the subscriber base had grown to 117.8 million. An updated version was launched in 2025, extending access to offline bank branches for elderly users and dropping the minimum sign-up age to 14.

AI banking – The next steps

Both KakaoBank and Toss are now pursuing AI banking strategies, but from different angles. KakaoBank is building toward what CEO Yun Ho-young calls “AI-native banking.” In 2025, it launched South Korea’s first Azure OpenAI conversational search in financial services, an AI Financial Calculator for natural-language queries, and AI Transfer, the country’s first conversational money transfer service. Kakao Group has also announced plans for a Korean won stablecoin ecosystem that connects KakaoPay, KakaoBank, and KakaoTalk to a unified digital wallet that will allow users to make peer-to-peer payments without intermediaries.

Toss has taken a different approach and is focusing on security and authentication. In 2023, the company’s AI fraud detection system could identify fake identity documents at account opening with over 94% accuracy. In 2025, the company launched Facepay – a face-scanning payment system for physical stores that requires no card or PIN. Where KakaoBank is building an AI-native bank, Toss is building an invisible security infrastructure.

Tensions and challenges

South Korea’s digital banking model is not without its challenges. According to World Bank research, the leading open banking app accounted for 47.9% of all open finance API calls in May 2023. This means that a single outage, breach, or change in business model has the potential to disrupt almost 50% of the country’s open finance ecosystem, it added.

Digital exclusion of older users also remains a challenge, despite some progress. KakaoBank’s penetration among the over-60 age group has risen from 12% to 15%, while MyData 2.0’s offline expansion is a direct response to the limits of a purely app-based model.

The question France must ask

The success of South Korea’s open banking model raises a direct question for French banks: does consumer trust precede adoption, or does adoption create trust?

In South Korea, KakaoTalk was already on 95% of Korean smartphones before KakaoBank was launched. The trust was already there, making KakaoBank viable from the day of its launch. In France, neobanks such as Lydia and Qonto have started with no equivalent depth of trust. Is there a daily-life app in France with the same everyday usage as KakaoTalk or even China’s WeChat? The answer remains open.

For more expert content on industry outlooks and innovation, subscribe to our newsletter or visit our Insights page.

Q&A: Questions on South Korea’s open banking landscape

South Korea’s open banking system had 203 million registered accounts at the end of 2024, about four times the population, as citizens can hold multiple accounts across different banks and services. This is a result of the country’s financial product usage and digital infrastructure built over more than two decades.