Wholesale and floor plan operations in automotive and equipment finance rely on auditing methods to safeguard their funded assets. And with the equipment finance market valued at approximately $1.34 trillion and automotive finance at around $295 billion, even small control gaps can translate into material losses at scale. Historically, physical, on-site audits have formed the backbone of governance in asset finance, with auditors visiting dealerships to verify inventory and controls. However, evolving fraud techniques, increasing portfolio complexity and heightened regulatory scrutiny are exposing the limits of purely physical audit models.

As lenders reassess how best to balance cost, coverage and risk, audit strategies are beginning to shift towards more flexible, blended models. In this article, we explore why hybrid auditing is gaining traction and how it addresses the structural challenges facing traditional audit frameworks.

Physical auditing in 2026

Technology has become an essential tool for improving operational resiliency, efficiency and customer relationships; however, it cannot fully replace the human touch. The decades of experience held by physical auditors remains highly valuable, particularly their ability to assess complex situations, detect subtle anomalies and conduct in-person verification. Many risk frameworks emphasize regular audit cycles as critical to balancing risk.

Until recently, physical audits were widely trusted as the primary safeguard across asset finance portfolios. But as portfolios scale and risks evolve, this longstanding approach has struggled to keep pace. The strength of physical auditing lies in depth rather than scale, which has become a growing challenge, especially for lenders who manage thousands of assets across different locations.

The challenges of physical auditing

One of the main challenges of physical audits is their impact on business resources. Direct costs include travel, accommodation and staffing, while indirect costs arise from scheduling delays caused by illness, staff vacation, weather disruptions and travel constraints. These delays can result in weeks or even months between audit visits, creating blind spots in which fraud can go undetected and escalate.

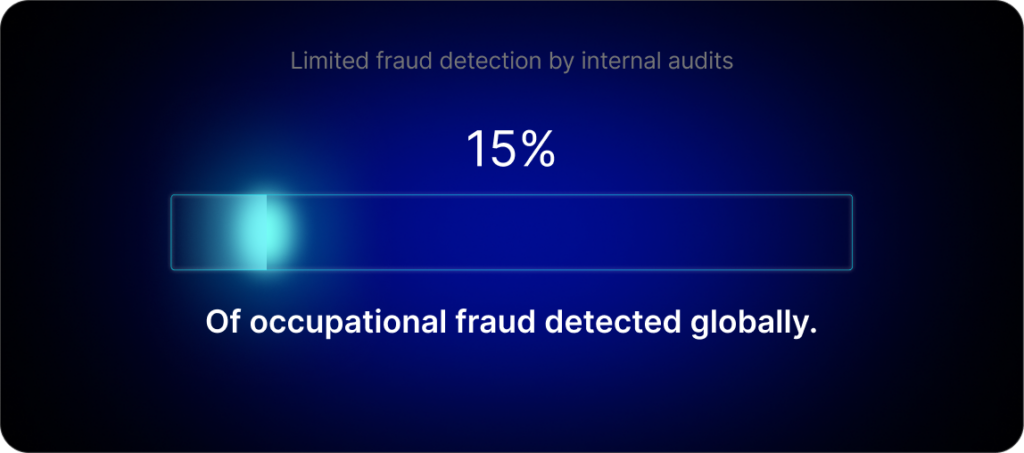

Across all markets globally, internal audits only detect around 15% of occupational fraud, per the Association of Certified Fraud Examiners (ACFE), who also state that a typical fraud case can last over 12 months before detection. Per the ACFE’s report, most instances of fraud are detected through employee tip-offs, accounting for three times more than the next common method. The United States and Canada account for 38% of reported cases, with the next largest region (Sub-Saharan Africa) representing 18%.

When organizations rely on internal reporting between physical audits, detection depends heavily on chance, someone being in the right place, at the right time and taking the right action. As audit intervals lengthen and reliance on informal detection increases, the risk is not simply delayed visibility, but prolonged exposure to undetected loss.

Potential loss exposure

These gaps in audit coverage have direct and material financial consequences. When fraud or asset misrepresentation goes undetected between physical inspections, losses can accumulate rapidly, often before lenders have an opportunity to intervene.

Recent high-profile cases, such as the Tricolor Auto collapse, illustrate the impact of governance failures and how fraud can devastate businesses. In late 2025, Tricolor Auto’s CEO and three others were charged with defrauding lenders, with significant ripple effects for the wider industry. JP Morgan disclosed that it had taken a $170 million loss from Tricolor.

This is just one example. At the start of 2025, auto finance fraud was reported to have increased by 16.5%, year over year, reaching a record $9.2 billion. While identity fraud accounts for part of this increase, a significant proportion relates to income and employment misrepresentation. Asset finance organizations face multi-directional fraud risks, making early detection and mitigation critical. Together, these dynamics highlight the limitations of audit models that rely on periodic, resource-intensive inspections alone.

Balancing risk vs cost

When addressing fraud exposure, organizations must balance available resources against potential risk. Traditional physical audits incur high costs, limiting frequency and delaying detection. These are conditions under which fraud and asset misrepresentation can escalate rapidly.

At the same time, reducing audit coverage to control cost introduces its own risks, leaving lenders exposed to longer detection windows and weaker oversight across distributed portfolios. This tension between cost efficiency and risk mitigation has become increasingly difficult to manage as asset volumes and geographic dispersion increase.

In response, organizations are beginning to supplement physical audits with digital capabilities that extend coverage between site visits. By increasing audit touchpoints without materially increasing cost, digital tools help narrow detection gaps while preserving the depth and judgement of physical inspections where they are most needed.

What is hybrid auditing?

In response to these challenges, asset finance organizations are increasingly reassessing how audit coverage is delivered. Rather than relying solely on physical site visits, many lenders are exploring approaches that extend verification between inspections without compromising audit integrity.

Hybrid auditing is a process that combines the expertise of physical auditors with digital auditing tools, enabling dealerships to complete self-service audits between visits. This can be done as frequently as needed by an organization and provides a practical way to monitor locations with higher risk scores.

This approach delivers the accuracy and investigative strength of physical audits alongside the scalability, efficiency and cost benefits of digital verification. Physical auditors can then be strategically deployed to high-risk sites, while digital tools manage routine verification and provide near real-time insights.

| Audit approach | Coverage & frequency | Cost efficiency | Risk detection capability | Operational flexibility |

| Physical auditing | Periodic, site-based inspections limited by travel and scheduling | High cost per audit | Strong depth and judgement at point of visit | Limited scalability across large or dispersed portfolios |

| Digital auditing | High-frequency, remote verification between visits | Low cost per audit | Effective for routine checks and anomaly flagging | Highly scalable across locations and geographies |

| Hybrid auditing | Continuous coverage combining site visits and remote checks | Balanced cost model | Combines human judgement with ongoing detection | Flexible deployment aligned to risk profiles |

From insight to implementation: How SBS can help

SBS has been a longstanding champion of hybrid auditing through digital tools. Every year, nearly 60,000 digital self-service audits are completed across more than 18,000 active locations. In 2024, our digital audit tool processed nearly 3 million images. The SBS Digital Audit is trusted by industry leaders and incorporates technology designed to prevent image and location manipulation, while allowing organizations to customize audits to their specific requirements. A low cost-per-audit pricing model enables lenders to deploy self-service inventory audits as frequently as needed, across any geographic region.

Recognizing that effective audit strategies are rarely one-size-fits-all, SBS works with Alliance Inspection Management (AiM) in the United States, while also supporting integration with other physical audit providers globally. This approach enables lenders to retain their existing audit partners, centralize data and scheduling within a single platform, and scale digital audits alongside physical inspections to achieve balanced, risk-aligned coverage. To learn how hybrid auditing can strengthen oversight while balancing cost and coverage, contact us today to discuss your audit strategy and explore how a tailored hybrid approach could support your organization’s risk and compliance objectives.

Questions & Answers

Why are traditional physical audits no longer sufficient on their own? + –

Physical audits provide valuable depth and professional judgment, but their cost and logistical constraints limit frequency. This can create extended gaps between inspections, increasing exposure to undetected fraud and asset misrepresentation.

Does digital auditing replace physical auditors? + –

No. Digital auditing is designed to complement, not replace, physical inspections. It extends coverage between visits, allowing auditors to focus their time and expertise on higher-risk locations.

How does hybrid auditing improve fraud detection? + –

By increasing audit touchpoints and reducing detection windows, hybrid models help surface issues earlier, before losses escalate, while preserving the investigative strength of in-person audits.

Is hybrid auditing suitable for all asset finance portfolios? + –

Hybrid auditing is adaptable to different portfolio sizes, geographies and risk profiles. Audit frequency and coverage can be tailored, making the model suitable for both complex, high-volume portfolios and more targeted use cases.