As the world continues its digital transformation, the European Central Bank (ECB) is moving cautiously toward the possible launch of the digital euro – a central bank-issued currency that offers a universal, secure payment method for everyday use. The ECB’s two-year preparation phase to explore the possibility of a central bank digital currency (CBDC) began in November 2023 and is expected to end in October. Since then, the bank has established the foundations for the potential issuance of the digital euro. This includes public and stakeholder consultations, a draft rulebook, extensive testing and experimentation, and selecting providers to develop a digital euro platform and infrastructure.

However, numerous challenges remain, including privacy concerns, the complexity of political and technical coordination across the 27-member EU, a lack of compelling use cases for consumers, as well as competition with existing digital payment solutions such as cards and wallets. Despite the challenges, the EU is not alone in pursuing the possibility of a CBDC. According to data by the US-based think tank the Atlantic Council, 134 countries, representing 98% of the world’s gross domestic product, are exploring CBDCs – up from only 35 in 2020.

Countries including Australia, Japan, India, Brazil, and Turkey have already entered the pilot stage of launching CBDCs, while three countries – the Bahamas, Jamaica, and Nigeria – have fully launched a digital currency. Meanwhile, China’s digital yuan is the largest CBDC pilot in the world, with transaction volumes reaching 7 trillion e-CNY ($986 billion) in June 2024, the Atlantic Council data shows.

Why a digital euro?

The push for a digital euro has been driven by a rapid change in how Europeans pay for everyday transactions. The use of cash has been decreasing steadily over the past five or so years, particularly with point-of-sale transactions, while there has been a surge in digital, mobile, and card-based payments in its place. According to a 2024 ECB study on the payment attitudes of consumers in the euro area, 52% of transactions were made in cash last year, down from 59% in 2022 and 72% in 2019. As a result, the proportion of card payments jumped from 34% in 2022 to 39% in 2024, and online payments rose to 21% in 2024, up from 7% in 2019. While mobile payments remain low, they have doubled to 6% since 2022, according to the study.

However, a growing number of transactions are processed through third-party infrastructure, with much of it owned by non-European payment providers. And it is this issue that has prompted the ECB to consider its own CBDC to reduce Europe’s dependence on non-European card networks and digital wallets. A digital euro would also support Europe’s strategic autonomy and monetary sovereignty by making the payments landscape more competitive and resilient to foreign payment providers, according to a statement by the ECB.

“A digital euro would make our lives easier by giving us the choice to pay with a secure means of payment universally accepted throughout the euro area,” it adds.

Modern convenience with the digital euro

Unlike cryptocurrencies, a digital euro would be issued and backed by the ECB, which means it is guaranteed to retain its value. It is intended to function alongside cash and to be accessible to everyone across the euro area.

“Cash will continue to be a payment option; it will not be replaced. At the same time, to ensure that our currency remains future-proof, it needs to evolve in line with people’s payment preferences,” the ECB says.

The proposed features of the digital euro include legal tender status across the euro area, free access for citizens, offline payment functionality for resilience and privacy, and full interoperability with existing banking infrastructure. The dual approach of physical cash and the digital euro is designed to provide continuity, choice, and financial inclusion, according to the ECB.

“A digital euro would give European consumers a simple and safe digital payment option, free for basic use, that covers all their payment needs everywhere in the euro area,” Piero Cipollone, a member of the ECB’s executive board, said during a recent speech at the France Payments Forum in Paris.

A study by the ECB on consumer attitudes toward a CBDC found that close to half of respondents would be likely to use the digital euro, Cipollone added. The ECB research is in line with a Bundesbank survey, which found that about 50% of Germans were open to the idea of a digital euro. However, the survey also revealed that 59% of respondents were unaware of the digital euro, while 15% believed it was intended to replace cash.

Key concerns and challenges

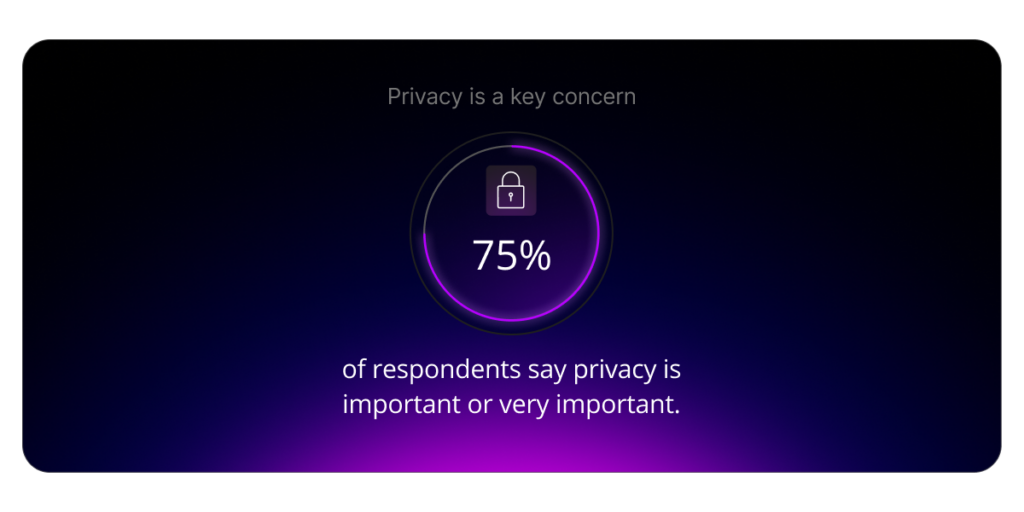

Privacy remains a top concern for members of the public. The ECB survey shows that over three-quarters of respondents believe strong data privacy should be a key feature of the digital euro. It was a similar response in the Bundesbank survey, with more than 75% of respondents rating privacy as important or very important when it comes to the digital euro.

Striking a balance between offering “cash-like” anonymity will be a challenge for the ECB as it also has to ensure that it complies with anti-money laundering (AML) and fraud-prevention regulations. Ensuring the digital euro is built on European-owned infrastructure is also important to safeguard data sovereignty and control over key financial systems. The ECB is also considering holding limits to ensure the digital euro functions primarily as a medium of exchange and not a store of value to prevent financial instability and bank runs.

Next steps

The ECB’s progress has been steady, and several processes are currently underway, including a review of legal frameworks, the testing of conditional payments and offline capabilities, and ongoing consumer research. During his speech in Paris, Cipollone said about 70 merchants, fintechs, start-ups, banks, and other payment service providers were working alongside the ECB to explore the potential of the digital euro to drive innovation.

“In July, we will release a report on these innovation partnerships,” he said. “It will include the technical information shared with the participants, enabling the entire market to replicate these activities, thereby further supporting innovation by the private sector.”

However, Cipollone also indicated at the conference that the ECB hoped to have all the political decisions in place by early next year, according to a report by Reuters.

“I hope to have everything done by the beginning of next year, very early next year,” Reuters reported Cipollone as saying. “We need the legislation in place, and from that, two to three years will be enough to launch the digital euro.”

The digital euro remains an evolving, “complicated” project that aims to balance the convenience and innovation of electronic payments with Europe’s commitment to cash, privacy, and financial stability. However, it must first overcome the numerous challenges – privacy concerns, developing a compelling case for consumers to switch to a digital euro, as well as uniting the single bloc on a political and technical level.

A digital euro has the potential to become a symbol of Europe’s financial sovereignty, offering citizens a secure and inclusive alternative to foreign-owned payment providers, digital wallets owned by tech giants, and unstable cryptocurrencies. While that future is possible, it will only happen if the digital euro earns what physical cash has taken centuries to build: widespread public trust.

For more expert content on industry outlooks and innovation, subscribe to our newsletter or visit our Insights page.