Digital identity (ID) systems are fast becoming an essential element to future-proof global economies, allowing citizens to securely access a range of public and private platforms to carry out everyday activities – from banking and healthcare to paying taxes and signing documents. In the banking sector, digital IDs offer users more secure and inclusive financial services, streamline customer onboarding, verify mobile banking transactions, reduce fraud, and enhance customer support channels.

Around the world, digital IDs are replacing the traditional username and password process with a broader set of security-enhanced elements, such as personal information, biometric details, behavioural data, and device identifiers. According to a report by the World Bank, digital IDs are recognized as the “linchpin of a trusted digital public infrastructure foundation, enabling reliable authentication and trusted interactions between individuals, governments, and businesses.”

Driven by the world’s rapid digitization since the Covid-19 pandemic, the introduction of stricter compliance requirements and continuing efforts for financial inclusion, numerous governments and the private sector have already embarked on building their own digital ID frameworks.

What is BankID and why has It become Sweden’s digital identity standard?

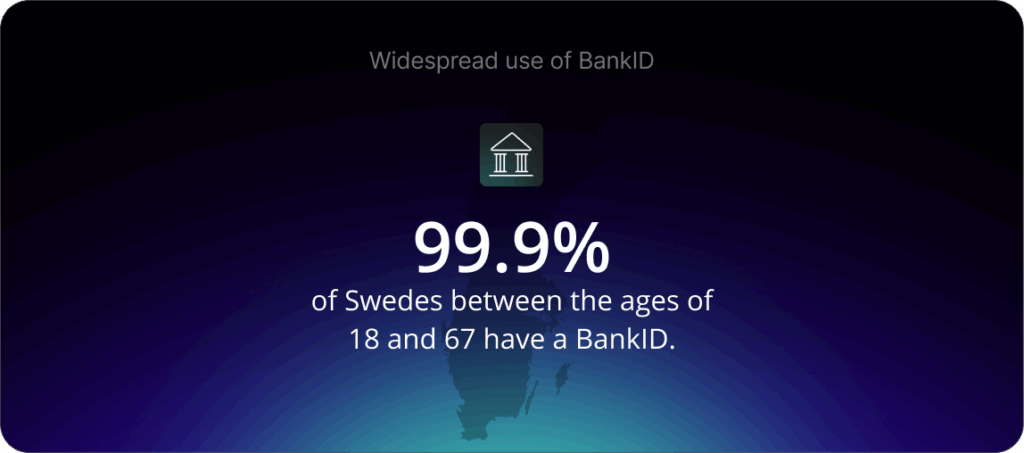

One of the world’s most widely used digital ID systems is Sweden’s BankID. Launched in 2003, it is operated by a consortium of seven Swedish banks – Handelsbanken, Swedbank, SEB, Längsförsäkringar Bank, Danske Bank, Skandiabanken, and Ikano Bank – and was used 7.6 billion times in 2024 alone, BankID data shows. As of 2024, more than 8.6 million Swedes between the ages of 18 and 67, or 99.9% of adults, used BankID to access 7,500 services across private and public sector platforms.

The widespread adoption of BankID reflects Sweden’s digital-first approach to public and private services. The system has effectively replaced traditional paper-based identification methods for most online interactions, creating a unified authentication standard that benefits both service providers and citizens. This remarkable penetration rate demonstrates how effective public-private partnerships can drive digital transformation at a national scale.

How does Sweden’s BankID system work?

BankID is a digital proof of identity, enabling users to verify who they are securely when accessing online services or signing documents. Issued by participating banks, the system links a user’s personal identity number to their BankID credentials, which are stored on a smartphone app, computer or a physical card.

To obtain a BankID, users must have a Swedish ID number and an account with one of the consortium banks. The onboarding process includes either in-person or digital verification, which is required under Sweden’s anti-money laundering (AML) and know-your-customer (KYC) regulations. Once active, BankID can be used across a range of platforms, such as logging into government portals or mobile banking apps, authorizing medical record access, paying taxes, or signing documents. Authentication involves biometric approval or a six-digit code that users receive through the BankID app.

Secure and compliant

BankID’s success relies on a security infrastructure built on mutual Transport Layer Security (TLS) and is aligned with Sweden’s regulatory framework, such as AML and data protection standards. It also employs encryption, device binding, and multi-factor authentication to reduce fraud and ensure only verified users can gain access to the system.

BankIDs are linked to users’ devices and their ID numbers, which cannot be shared or duplicated. Biometric authentication, such as fingerprint or facial recognition, adds another layer of security. For sensitive transactions, users must also scan their passport or ID card via near-field communications during the authentication stage. The system meets Sweden’s Financial Supervisory Authority requirements and enables Advanced Electronic Signatures (AES), which complies with the EU’s eIDAS regulation and gives signed documents full legal value.

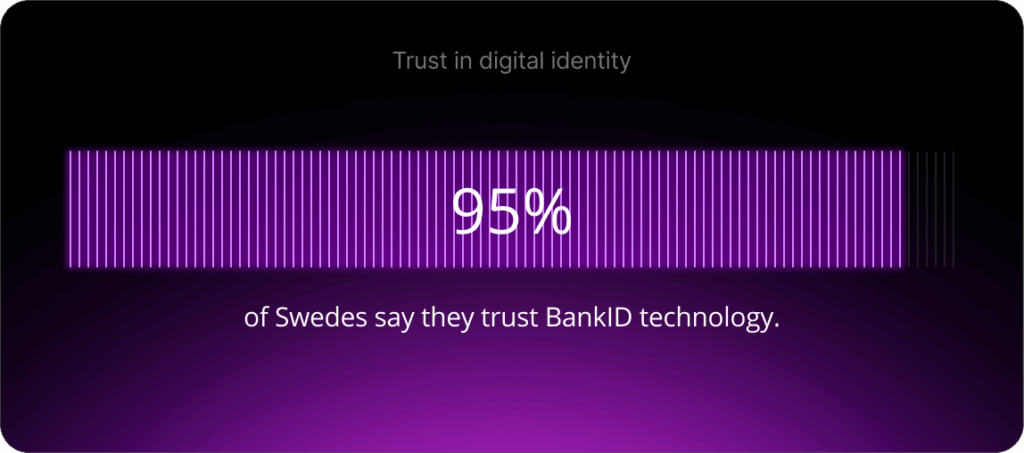

Banks and fintechs that use BankID also benefit from the shared infrastructure, which has simplified KYC processes and limits their exposure to identity fraud. According to a 2024 survey, users benefit from a seamless experience while conducting their daily affairs online, leading to a high level of trust in the technology. The survey found that a majority of Swedes consider BankID to be their most important app, and 95% of the population says they trust technology.

What impact has BankID had on Swedish banking?

BankID has become a key driver in the digital transformation of Sweden’s banking sector by simplifying compliance, reducing operational costs, and enhancing the customer experience. BankIDs are used to verify a customer’s identity during the onboarding process, which complies with the country’s KYC and AML regulations without requiring paper documents or in-person visits. This has resulted in reduced account opening times and boosted fraud prevention through real-time, multifactor verification.

BankID is also playing a key role in the day-to-day delivery of financial services, allowing customers to log into mobile banking apps, authorise payments, sign credit agreements or apply for loans, thanks to its digital signature feature. From an operational perspective, the system supports standardized, secure integration across banking platforms, which allows financial institutions to embed authentication seamlessly into their digital workflows, reduces development times, and simplifies system maintenance.

The result? A more efficient and trusted digital banking environment, particularly as Sweden is on track to become the world’s first cashless economy.

How are other nations implementing digital ID systems?

Other countries have also introduced digital ID systems, although with varying degrees of success. Estonia is an early pioneer of the technology with its e-ID system, which has been integrated into nearly every aspect of the lives of its citizens.

India’s Aadhaar system uses biometric data to provide access to welfare and banking platforms. In contrast, Canada’s SecureKey Concierge and Nigeria’s NIN systems follow a decentralized model, in which multiple providers issue and manage digital identities under a shared trust framework.

Spain’s mobile-based MiDNI system currently allows users to access government services, but there are plans to expand it to include online ID verification and digital signatures, as well as for voting, opening bank accounts, renting cars, and even checking into hotels.

According to research by the McKinsey Global Institute, countries that implement digital IDs could unlock value equivalent to 3% to 13% of gross domestic product by 2030. However, concerns about privacy remain. And a report by Regula notes that widespread adoption of digital IDs requires a globally unified standard and shared frameworks, which could explain countries’ slower uptake of the technology.

What does the future hold for digital identity systems?

As the world’s digitalization continues to evolve, national digital ID systems are expected to expand beyond authentication for government and private sector platforms.

While platforms such as Sweden’s BankID have become essential digital services for millions of users, the next step for digital ID technology could be a deeper integration with super apps. This would create unified platforms that combine banking, payments, government services, messaging, financial products and other features within a single interface, similar to Spain’s plans for the future of its MiDNI system.

Sweden’s experience, meanwhile, offers valuable lessons for governments and financial institutions planning to implement their own digital ID frameworks – from the importance of public-private sector collaboration to building trust and enabling financial inclusion in delivering seamless, secure digital experiences for citizens.

For more expert content on industry outlooks and innovation, subscribe to our newsletter or visit our Insights page.

What makes BankID different from traditional online banking passwords? + –

BankID provides multi-factor authentication tied to your personal identity number and device, offering significantly higher security than simple username-password combinations. It also serves as a legally binding digital signature for documents and contracts.

Can tourists or temporary residents in Sweden get BankID? + –

No, BankID requires a Swedish personal identity number and an account at one of the participating banks. Temporary residents with personnummer can apply, but tourists cannot obtain BankID.

How does BankID protect against identity theft? + –

BankID uses device binding, biometric authentication, and encryption to prevent unauthorized access. Each BankID is uniquely tied to an individual’s device and cannot be duplicated or transferred without proper verification.