Regulatory reporting has become an increasingly sore spot for banks in recent years. Its scope has not only grown, it’s exploded. Multiple jurisdictions, post-crisis rules, transparency demands and sustainability reporting have all created unprecedented complexity, and banks are struggling to keep up. In fact, research shows that the portion of banks’ IT budget devoted to compliance grew by 40% between 2017 and 2023. Of course, banks don’t have a choice when it comes to following regulatory requirements or not. Fines, reputational damage and even banking licenses are at risk for financial institutions who fail to meet compliance standards.

However, compliance doesn’t have to be a never-ending headache. In fact, in building up the infrastructure and culture needed to meet regulatory requirements, banks are also building an invaluable dataset that will help them navigate other industry challenges, outpace competitors and provide better services to their customers.

Has financial reporting become unsustainable?

It’s no coincidence that financial reporting has become increasingly complex for banks. The world has changed, new technologies have become part of our day-to-day lives and customers expect more from their banks than they used to, not just in terms of how their money is managed, but the bank’s brand and reputation. Regulatory reporting has, in turn, evolved to ensure that banks are meeting these ever-changing needs.

- Overlapping jurisdictions. Banks operating in multiple regions must comply with both EU-wide regulations and local supervisory rules. These layers often overlap, creating duplication and inconsistency across templates, formats and reporting timelines.

- New rules after every crisis. Each financial or economic crisis brings a wave of new regulation. Over the past 15 years, events like the 2008 crash, the eurozone crisis and recent bank failures have led to hundreds of new reporting requirements, particularly around capital, liquidity and market risk.

- Greater expectations for transparency. Regulators are demanding more frequent and more detailed disclosures, not just to catch risks, but to improve governance and rebuild trust. This means more granular, auditable and timely data is expected from every institution.

- ESG & CSRD expanding into non-financial domains. Banks are now required to report on climate risks, green asset ratios and environmental impacts. CSRD, in particular, mandates that banks treat ESG data with the same rigor as financial reporting, a major shift in scope and complexity.

Rather than a sudden, one-off period of growth in regulatory change, this new constant acceleration is, in fact, the new normal. Banks can expect reporting to continue changing at a similarly rapid rate in the coming years due to the following regulatory trends likely to be put in place:

- Contract-level granularity from IReF & IRS. Future frameworks like IReF will require banks to report at the level of individual loans or securities, not just aggregates.

- Smaller banks pulled into Tier-1-level expectations. While large, systemic banks have faced complex rules for years, regulators are now extending the same standards to mid-sized and smaller banks, especially around capital, risk and ESG.

- Ad-hoc supervisory requests with days-long deadlines. Supervisors increasingly expect banks to respond to data requests on short notice. Reports that once took weeks to prepare must now be delivered in days, sometimes hours, requiring flexible, scalable data systems.

Turning compliance data into a strategic asset

Building an infrastructure and culture of compliance may seem to many banks like a daunting and unwelcome task, but turn it on its head, and it’s not hard to see it as an opportunity. By rising to the challenges posed by regulatory reporting, banks can achieve a variety of advantageous outcomes not directly linked to compliance.

- Capital & liquidity optimization. Regulatory data provides a clearer, more accurate view of the bank’s assets, risks and collateral. With better visibility, banks can avoid unnecessary capital consumption and redeploy capital into new financing.

- 360° customer insight. Reporting data shows how customers actually use products, repay credit and manage risk. Banks can use this to build stronger relationships and offer more relevant products based on real behavior, not assumptions.

- ESG & business development. Sustainability reporting reveals which clients and sectors are transitioning, and where green financing needs are emerging. ESG data becomes a guide for where future commercial opportunities lie.

- Competitive advantage. Regulatory data gives banks earlier clarity on what’s coming and how fast they must adapt. Institutions with strong data foundations respond faster to new rules, protect their reputation and bring compliant products to market sooner.

How can banks unlock regulatory data potential?

As any bank will tell you, meeting regulatory reporting requirements is difficult enough, and turning those changes into strategic advantages is even more challenging. Many banks are simply incapable of making the leap on their own. They face integral structural barriers, silos, legacy systems, manual processes and fragmented ownership.

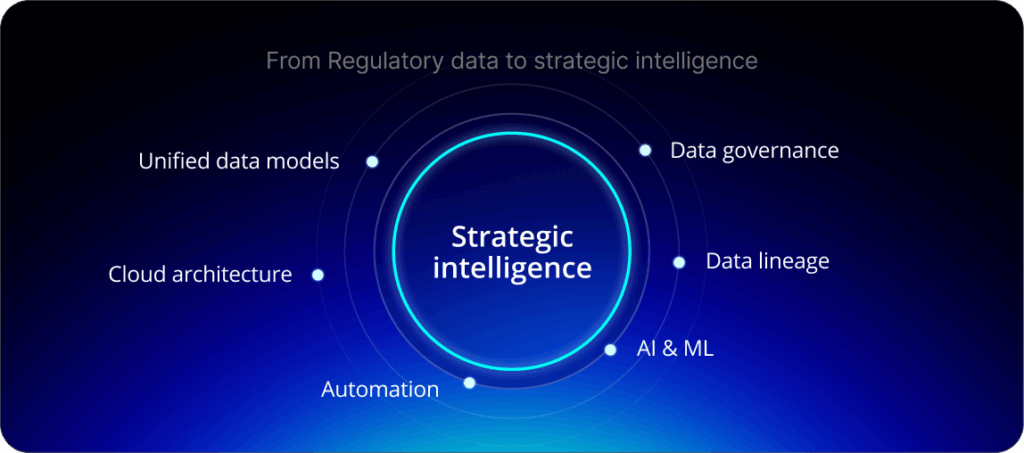

To turn regulatory data into strategic intelligence, banks need an overhaul in technological infrastructure, organizational culture and approach to data management. Below is a snapshot of how today’s common challenges can be transformed into future-ready capabilities:

| Barrier | Strategic enabler |

| Siloed, fragmented data systems | Unified data models: Report once, reuse everywhere |

| Legacy on-prem systems | Modern cloud architecture: Scalable, flexible, ready for granular data |

| Manual reporting processes | Automation & industrialization: Faster, cheaper, more consistent compliance |

| Reactive compliance culture | AI/ML augmentation: Predictive insights and anomaly detection |

| Poor data governance and ownership | Data lineage & governance: End-to-end traceability and control |

How SBS can help: Move your bank from reporting to intelligence

For banks to succeed not only in regulatory compliance but also turning that compliance into strategic advantage, banks must work with an experienced partner capable of navigating the regulatory landscape, not just now but in the years to come.

SBP RR is positioned as the platform that unlocks this new model of regulatory intelligence. Its key features include:

- Much faster time-to-compliance (CRR3 in 8 weeks vs 6–9 months)

- Up to 30% operational cost savings via industrialized reporting

- Scales from 60k to millions of data points without proportional cost increases

- Single data-model approach supporting analytics, reporting and cross-department use cases

These advantages will only become more important in the years to come. Regulation will continue to expand in scope, granularity and velocity. As such, banks face a choice, They can either treat reporting as an ever-growing cost, or unlock the intelligence embedded in regulatory data. By working with a trusted and experienced partner like SBS, banks can turn regulatory pressure into operational resilience, strategic foresight, and long-term advantage.

Reach out to a member of our team today and find out how to navigate regulatory change at your bank.

How much are banks currently spending on regulatory compliance? + –

According to recent research, banks’ IT budgets for compliance rose by approximately 40% between 2017 and 2023, reflecting the growing complexity and scope of regulatory requirements.

What are the main regulatory challenges banks face? + –

The primary challenges include overlapping jurisdictions, continuous new regulations following financial crises, increased transparency demands, and expanding ESG/CSRD requirements that treat sustainability data with the same rigor as financial reporting.

Can smaller banks avoid complex regulatory requirements? + –

Regulators are increasingly extending Tier-1-level expectations to mid-sized and smaller banks, particularly around capital, risk, and ESG reporting. The trend shows that regulatory standards becoming more uniform across all bank sizes.

How quickly must banks respond to regulatory requests? + –

Supervisors increasingly expect responses within days, sometimes hours, for data requests that previously took weeks to prepare. This requires flexible, scalable data systems.

What strategic benefits can banks gain from compliance data? + –

Banks can achieve capital and liquidity optimization, gain 360-degree customer insights, identify ESG business opportunities, and establish competitive advantages through faster adaptation to new regulations.