In recent years, consumers’ expectations of their providers have evolved. Netflix and Disney+ recommend television shows tailored to viewers’ preferences. TikTok’s algorithm curates content aligned with their interests. Amazon suggests new products to users based on their browsing and purchase patterns. Consumers increasingly bring the same expectations to their financial relationships as they do to other services. While financial institutions are not mind readers, they can use available data to understand consumer intent and anticipate future needs.

Banks, building societies and lenders around the world already have access to exactly the tools they need to provide a more tailored experience to account holders, data. Many institutions have recognised this and are advancing their personalisation strategies, while some are evaluating their next move.

Predicting life events

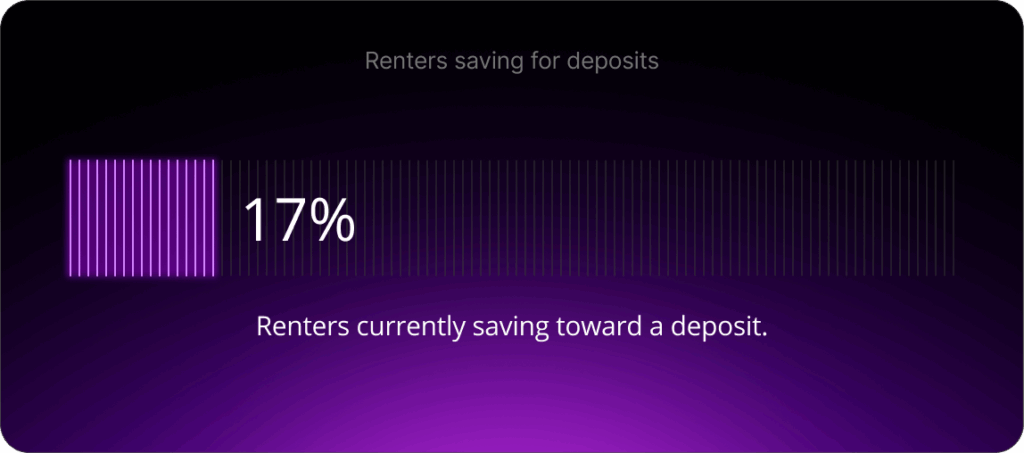

A recent Barclays Property Insights report found that 17% of renters were saving for a deposit, but how can banks or building societies identify this behaviour using data?

Let’s think about this as an example. Consider Thomas and Fatima, who have been renting a property together for five years. They have recently begun contributing to a joint savings account with the goal of purchasing their first home. While their bank may not know these details, available data can reveal indicators that major life events are approaching. By analysing these signals, the bank can anticipate their needs and deliver a more personalised experience.

The purchase of a first home can be identified through potential data indicators

- Thomas and Fatima have consistently been paying rent for several years.

- They have saved an average of £300 per month for the past two years, totalling £7,200. At this rate, they are on track to reach a typical deposit amount within five and a half years.

- Fatima, who is 32 years old, has an additional Lifetime ISA (LISA) account with a balance of £14,000.

What data tells the bank

- Fatima opens 75% of marketing emails from the bank, while Thomas does not.

- Both are regular users of mobile banking services, accessing their savings account around 2.5 times per month each.

- Historic internal data tells the bank that savers are displaying similar patterns are often preparing to purchase a home:

- LISA savers under the age of 45 are most likely to use the funds to purchase their first home.

- On average, couples living in their area contribute a £20,000 deposit, with savings above £10,000 typically linked to home-buying goals.

What the bank could do next

- The bank could put Thomas and Fatima into a communications plan based on data analysis that focuses on turning savings into a home deposit, amounts needed for a deposit and mortgage products offered.

In addition to saving for a home, Thomas and Fatima had been setting aside smaller amounts in a separate holiday fund. However, plans have recently changed as they prepare for the arrival of their first child, using these funds to purchase items for a nursery.

Indicators of life changes

- Thomas and Fatima have a savings account named “Australia!” with a balance of around £3,000.

- Recently, they have started to draw this money out of savings at a rapid rate for several transactions valued at around a few hundred pounds each. These funds are transferred into a normal current account.

- At the same time, several purchases have been made at high-street baby stores for similar amounts.

What data tells the bank

- This account is likely no longer being used for its original purpose. Recent purchases of baby-related items suggest the couple may be preparing for a child.

What the bank could do next

- While assumptions should be avoided, the bank can share relevant information. For instance, communications highlighting different savings account options could subtly reference accounts for children, allowing the bank to gauge engagement with that content.

Thomas and Fatima could benefit not only from other products and services within their bank’s portfolio, but also from financial education initiatives to help them better manage and maximise their savings as their circumstances evolve.

Not all life events are positive

Harry has begun switching utility and insurance providers and cancelling direct debits. After his car recently broken down, he has struggled to make ends meet while saving for repairs, becoming increasingly price-sensitive. Data from Harry’s bank makes it clear that he is looking for price comparisons and adjusting his monthly outgoings. His bank could respond by sharing promotional material on discounts for car and home insurance, as well as information about their competitive instant-access savings rates.

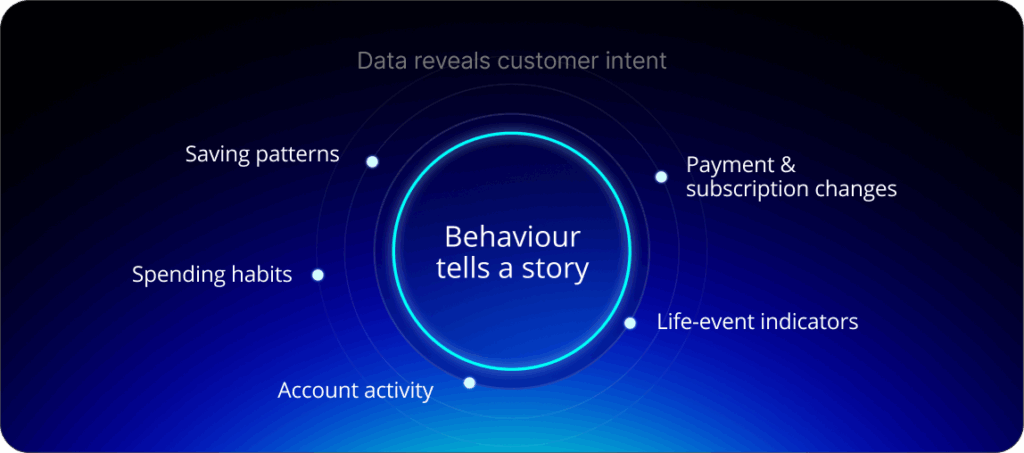

Recognising that Harry may also benefit from financial literacy materials, the bank could include him in a communication plan offering resources to support more informed financial decisions and directing him towards available assistance. As we have seen from the above examples, data points are not simply operational. They tell us a story about customer behaviour, priorities and readiness for change.

Integrating AI & machine learning

Spotting these trends across tens or even hundreds of thousands of accounts is not an easy task. However, the potential impact of timely, relevant communication makes this a logical and valuable step toward greater personalisation. In these examples, data insights could help Thomas and Fatima navigate purchasing their first home as they become parents. They may ultimately decide it is in their best interest financially to wait another year and put more money into Fatima’s LISA. Harry could adopt new habits that strengthen his financial resilience and readiness for future challenges.

While banks can promote new products and services, they can also help to improve retention. Gone are the days when consumers stay with one supplier for the entire life of their mortgage. The modern consumer looks for the best deal and the easiest platform to use. And, ultimately, they stay with a provider who makes them feel valued. As this trend evolves, regulation will likely strengthen to ensure organisations avoid bias, treat customers fairly and design products that align with their best interests. Consumer Duty principles will continue to guide the development of such practices.

The future of predictive banking

Mortgages and savings accounts have come a long way since the turn of the century. Hyper-personalisation has enabled banks, building societies and other lenders to offer new products and services, as well as find innovative ways to service their clients faster and more efficiently. Open banking offers a new world of visibility on customer behaviour and affordability, offering valuable insight when assessing creditworthiness.

As predictive banking matures, consumer expectations will continue to rise. We can expect broader use of embedded finance, predictive insights, real-time risk assessment, fraud detection and conversational banking assistants offering tailored financial guidance. Financial institutions that harness data responsibly and proactively anticipate customer needs will define the next era of banking, one built on trust, personalisation and financial empowerment. Banking will move beyond managing money to guiding individuals toward better financial decisions, informed by their personal circumstances.