The rate of bank branch closures in Australia has increased significantly since the 1980s, driven initially by the sector’s deregulation and privatization of state-owned banks. More recently, however, the shift to digital banking has led to more closures as Australians increasingly embrace cash-free lives and mobile banking. In 1993 alone, the country boasted over 7,000 bank branches, ranging from urban areas to rural towns. But by the early 2000s, that number had dropped by nearly one-third to 4,790.

Since 2017, more than 2,100 bank branches have been shuttered, marking a 39% reduction in active branches for major metropolitan areas and significantly impacting rural and remote Indigenous communities, according to a federal senate enquiry into the country’s branch closures.

What began as a slow retreat more than 40 years ago has reshaped the structure of Australia’s banking system as the country’s Big Four banks, the Commonwealth Bank (CommBank), Westpac, ANZ, and National Australia Bank (NAB), chased profits and closed bank branches. The Big Four now dominate the sector, controlling more than 70% of the market with combined assets of more than A$3.8 trillion, data compiled by InfoChoice shows.

Current state of Australia’s banking market

Today, Australia’s banking sector is worth more than A$5.3 trillion in terms of assets under management (AUM). CommBank leads the pack as the country’s biggest bank, with AUM of A$1.14 trillion and 15.9 million customers. This is followed by Westpac (A$1.08 trillion AUM and 12.7 million customers), NAB (A$905.3 billion AUM and 8.5 million customers), and ANZ (A$756.43 billion AUM and 8.5 million customers).

CommBank has also captured the biggest market share of banking customers at 14.3%, while Westpac has about 11.6%, NAB holds 9.8% of the market and ANZ is at about 8.8%.

But the banking sector is facing competition from FinTechs, as Australians embrace new ways to make payments and transfer money, thanks to the likes of buy now, pay later platform Afterpay and cross-border payments app Airwallex. Valued at US$4.1 billion in 2024, the sector is expected to grow by a compound annual growth rate of 8.9% to reach US$9.5 billion by 2033, according to research by IMARC Group.

One of the biggest financial services markets in Australia is the superannuation sector, which is valued at $3.9 trillion, according to a report by KPMG. Known as “super”, it is a mandatory savings vehicle for retirement in Australia, in which employers contribute at least 12% of an employee’s salary to their chosen super fund every quarter. The funds can be withdrawn at retirement age and are separate from the government’s age pension scheme.

Digital Identity and banking innovation

The growth of the banking and financial services sector has also been boosted by the 2023 launch of ConnectID, a national digital identity system designed to build a more trustworthy digital economy and protect Australians from fraud and identity theft, including banking and financial services customers.

Bank@Post: A solution to branch closures

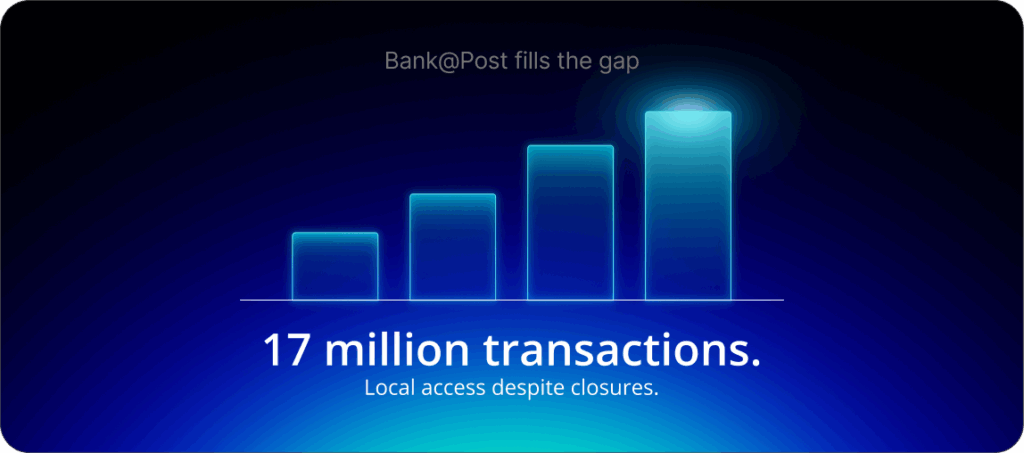

But as the digital transformation and closure of physical bank branches continue at a rapid pace, another service has emerged. In 1995, the federal government’s Australia Post began offering basic banking services through giroPost. Now known as Bank@Post, it serves consumers across the country and has helped to offset the impact of branch closures. According to Australia Post’s latest annual report, there were more than 17 million Bank@Post transactions in 2024 alone, including cash withdrawals and deposits amounting to about A$10 billion.

In our Banking is Local series, we explore the rise of Bank@Post, which has grown into a unique model of financial access that combines public infrastructure with private banking partnerships.

Impact on rural and indigenous communities

Australia’s branch closures have affected rural and remote Indigenous communities, particularly for people who lack reliable internet access or do not have the digital literacy skills to manage their finances online.

While many Australians have embraced digital banking – 80% prefer to check balances, pay bills, and transfer money online, according to Australian Banking Association (ABA) data – others do not have the tools or confidence to go fully cashless.

However, the lack of bank branches in rural and remote areas means that communities have lost vital access to income support, bill payments, and face-to-face assistance.

For small businesses, community groups, and local service providers, the loss of physical banking options in rural and remote communities has added time, travel, and complexity to routine transactions.

Enter Bank@Post

As physical bank branches continued to rapidly close across Australia, a new solution began to take shape – Bank@Post, which allows customers to conduct basic banking transactions, such as cash withdrawals, cash and cheque deposits, and bill payments at participating post offices. Today, more than 3,300 post offices around the country offer Bank@Post services, including in more than 1,800 rural and remote areas. The service enables users to access more than 80 banks and financial institutions, such as CommBank, Westpac, and NAB.

ANZ joined Bank@Post in 2025, while Australia Post is currently in talks with Macquarie Bank and global giant HSBC to join the service. According to the Reserve Bank of Australia (RBA), 95% of Australians now live within 5.9km of a Bank@Post outlet, compared with 12km for authorised deposit-taking institutions (ADI) branches and ADI-owned cash machines.

“Despite the significant reduction in bank-owned cash access points since 2017, the distance that most Australians have to travel to reach the nearest cash withdrawal point has not changed markedly in recent years,” the RBA says in its January 2025 Access to Cash Bulletin.

“This is mainly because of the strong geographic coverage of Bank@Post and independently owned ATMs,” it adds.

While Bank@Post does not offer full-service banking, it is free to use and plays an important role in filling the gap left by branch closures, with the local post office now the most accessible point for the basic financial needs of millions of Australians.

Consumer perspective

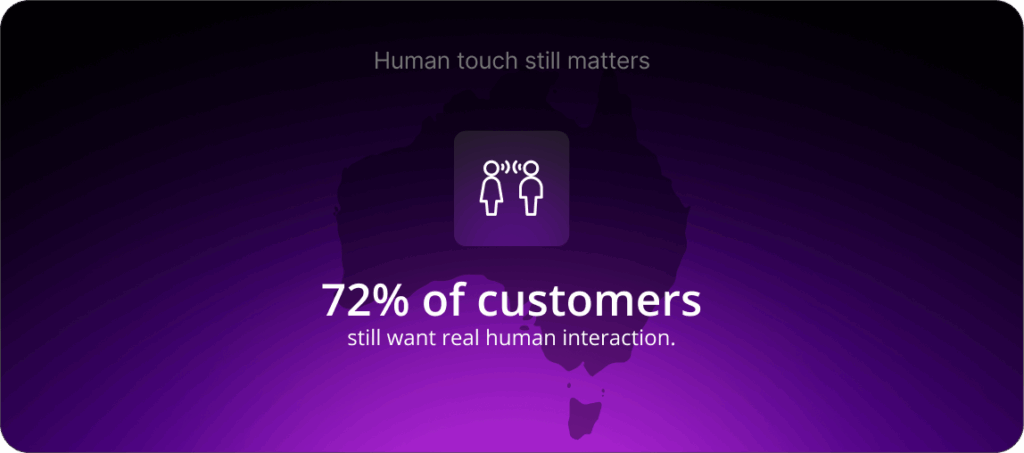

According to a survey by PwC Australia, 72% of respondents agree that they will always want to interact with a real person for at least some of their banking needs, while 39% of customers prefer to deal with complex banking tasks in person. Older Australians, those aged 55 and above, are more likely to equate face-to-face interactions with a great customer experience, PwC adds.

But data by Forrester shows that mobile is now the main banking channel for the majority of Australian adults. According to the report, 75% of banking customers now use banking apps on their smartphones to carry out transactions. Despite the rise in FinTechs and digital banking platforms, cash and in-person banking services remain vital for many rural and remote Indigenous communities, where digital access can be unreliable or non-existent. For these Australians, physical banking is not considered a backup, it remains the primary channel to manage their finances.

In more connected regions and metropolitan areas, many customers continue to value human interactions when it comes to their banking, particularly when resolving account issues or seeking personalised support and advice, as it provides a level of confidence and trust in their banks. However, by underpinning banking access in trusted local infrastructure, Bank@Post has helped to bridge modern banking with the realities of everyday financial management.

Global perspectives and future implications

Over the past four decades, Australia’s banking sector has transformed from a wide physical network of branches to a more consolidated digital model. While the benefits align with the global digital banking trend, the change has raised concerns about access and financial inclusion for all. The rise of Bank@Post has helped to overcome these challenges by using existing public infrastructure to extend private financial services to rural and remote communities that were in danger of being left behind by digital banking.

Similar questions are being asked elsewhere. In the UK, more than 6,000 branches have closed since 2015, prompting banks to redirect everyday services through the national Post Office network. In South Africa, the country’s four largest banks have collectively closed hundreds of branches in recent years, while mobile wallets are playing a growing role in helping people manage their finances where traditional infrastructure is limited.

As other countries face their own wave of branch closures, Australia’s Bank@Post model could provide a blueprint for managing and adapting to change, highlighting how innovation can bridge local relevance and the financial needs of consumers in a modern economy.

For more expert content on industry outlooks and innovation, subscribe to our newsletter or visit our Insights page.

Questions & Answers

What services does Bank@Post offer? + –

Bank@Post provides essential banking services including cash deposits, withdrawals, balance inquiries, and business banking deposits. These services are available through partnerships with 80 banks and financial institutions across Australia’s post office network.

Is there a fee for using Bank@Post services? + –

Bank@Post services are free to use for customers. The service is designed to provide accessible banking without additional charges, helping to maintain financial inclusion across all communities.

How many locations offer Bank@Post services? + –

More than 3,300 post offices across Australia offer Bank@Post services, with 1,800 of these located in rural and remote areas where traditional bank branches may no longer exist.

Which banks partner with Bank@Post? + –

Bank@Post partners with 80 banks and financial institutions, including the Big Four banks (CommBank, Westpac, ANZ, and NAB) as well as numerous smaller banks and credit unions.

Can I open a new account through Bank@Post? + –

While Bank@Post primarily handles transactions for existing accounts, specific account opening capabilities vary by financial institution. Customers should check with their preferred bank about account opening options through the service.