Since the 1970s, Vietnam’s banking sector has been dominated by state-owned commercial banks (SOCBs). However, it is now undergoing a digital transformation underscored by collaboration and innovation that is reshaping how millions of people access financial services. Super apps are playing a key role in Vietnam’s evolving mobile payments landscape. Driven by state and private sector partnerships, banks are teaming up with FinTechs to close the financial inclusion gap and extend access to financial services, particularly for the unbanked and underbanked in rural areas.

According to a recent report by EY, the government’s efforts, combined with a proactive stance by credit institutions, have led to significant improvements in the country’s financial ecosystem. Key to the sector’s growth has been partnerships between FinTechs and banks, EY adds.

“By working together, FinTech and banks are able to bridge the financial inclusion gap, with FinTech providing innovative platforms and customer engagement strategies, while banks offer trust, regulatory understanding, and financial infrastructure to support these services,” EY says in the report.

The State Bank of Vietnam (SBV), the country’s central bank, is working to advance the banking industry’s digital transformation agenda, issuing various regulations and creating legal frameworks and a favorable environment for financial inclusion goals. These include laws governing credit institutions, insurance businesses, anti-money laundering, and electronic transactions. Vietnam’s financial system – comprising the SBV, state-owned banks, commercial and foreign banks, insurance companies, FinTechs, microfinance institutions, and securities firms – is among the fastest growing in Asia. It accounted for a GDP value of 501.32 trillion Vietnamese dong (US$19.57 billion) in 2023, according to Statista data.

In our Banking is Local series, we explore the rise of Vietnam’s digital banking and mobile payments sector as it moves toward a cashless economy.

What is the history of Vietnam’s banking system?

Vietnam’s modern banking system emerged in 1976 with the formation of the SBV, shortly after the country was reunified. For the next decade, it functioned as a mono-bank system, a financial structure in which a single institution handles all banking activities.

However, in 1986, the country’s Đổi Mới reforms introduced partial market-oriented policies across the economy, opening the door to private banks and foreign institutions. While the so-called “Big Four” state banks—BIDV, Vietcombank, Vietinbank, and Agribank—dominate the sector, the country’s financial liberalization has continued. In March, the government increased the foreign ownership cap for certain domestic banks from 30% to 49%, Asean Briefing reported, adding that it came into effect on May 19, 2025.

“These institutions are expected to benefit from increased capital inflows, technological advancements, and enhanced governance structures as foreign investors take on larger stakes,” according to Asean Briefing.

Over the past decade, Vietnam’s state-owned banks have also been modernized through key reforms, notably equitization, which has boosted efficiency, transparency, and tech adoption. Although the process has been gradual, it has contributed to important changes in the sector, such as more autonomous management structures and stricter governance standards. It has also enabled state-owned banks to invest in new technologies and form partnerships with FinTech firms to accelerate their digital transition.

How are super apps transforming Vietnam’s financial landscape?

Perhaps the sector’s most significant transformation is the rapid shift to digital banking and mobile payments, driven by a young, mobile-first population, smartphone penetration, and strong government support for financial super apps.

The Covid-19 pandemic accelerated the cashless trend, driving a surge in online and contactless payments and enabling SOCBs and FinTechs to address service gaps, offer more online products, and align with the banking preferences of tech-savvy consumers.

According to analysis by Research and Markets, Vietnam’s mobile payments market is valued at US$40.5 billion. Despite the dominance of state-owned banks and centralized control, which have been tempered by the Đổi Mới reforms, super apps such as MoMo, ZaloPay, and VNPay are thriving within the framework, leading to a highly competitive mobile payments sector.

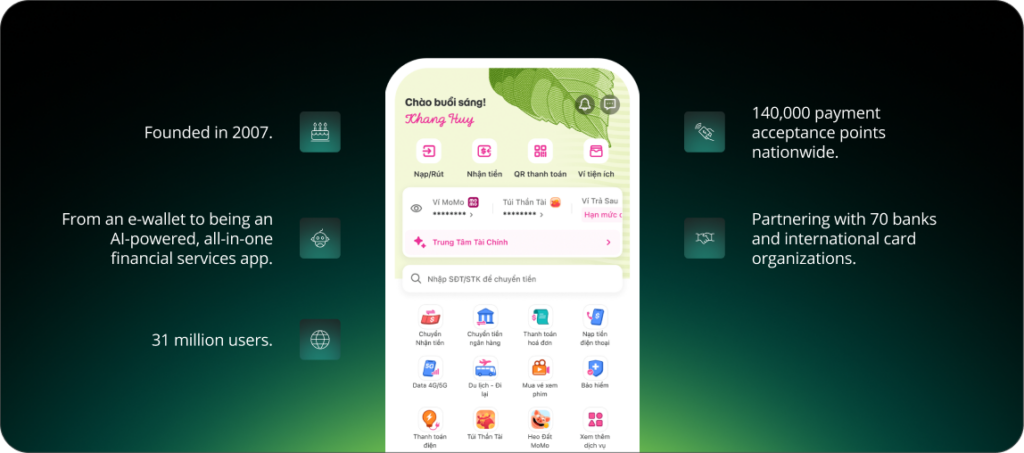

Founded in 2007, MoMo has helped to revolutionize the country’s mobile payments sector, evolving from an e-wallet to being an AI-powered, all-in-one financial services app that allows users to pay bills, conduct peer-to-peer transfers, apply for micro-loans and insurance products, invest and trade in stocks, as well as pay for groceries and other online services.

With more than 31 million users, MoMo has scaled rapidly since receiving its license from the SBV, expanding its network to include 50,000 domestic partners, 140,000 payment acceptance points nationwide, and partnering with 70 banks and international card organizations.

Why is the national QR code rollout important for Vietnam?

Meanwhile, MoMo – considered a unicorn FinTech after raising a total of US$434 million over five funding rounds – is also playing a key role in the government’s push to integrate digital payments with QR codes. The initiative comes under the National Payment Strategy, with the SBV aiming to achieve full interoperability between payment platforms by 2025.

While cashless payments are increasing in Vietnam, SBV statistics show that QR code transactions are the fastest-growing payment segment, resulting in the likes of MoMo adapting and repositioning itself as an AI-powered financial super app rather than an e-wallet, according to a report by Tech in Asia.

Thanks to frameworks such as the Law on Credit Institutions 2024, MoMo has been able to pilot a range of innovations, including e-KYC for credit applications, microloans, and embedded finance. The sandbox mechanism, overseen by the SBV, enables FinTechs to test and scale product features, which allows the central bank to grant licenses on a pilot basis, notes law firm YKVN.

What makes Vietnam’s super app model unique?

Momo’s rise as Vietnam’s leading super app is a result of the country’s approach to economic liberalization and state-led digital transformation. From early licensing to regulatory sandbox testing and aligning to national QR code strategies, it has become deeply embedded in the country’s economic ecosystem, particularly in rural and underserved areas. This hybrid model, which has modernized public access to banking while maintaining full regulatory compliance and financial inclusion, has created a FinTech that is more than a simple payment tool. Instead, MoMo has become an essential service for digital banking, public service access, and social equity.

Yet as super apps extend their role across credit, insurance, and even public services, they also raise important regulatory and societal questions. How will data protection, consumer rights, and competition be safeguarded in a market increasingly concentrated around a few dominant platforms? As Vietnam continues its journey toward a more inclusive, cashless future, the country’s banking evolution reflects a uniquely local approach – one that is being embraced by its tech-savvy population.

For more expert content on industry outlooks and innovation, subscribe to our newsletter or visit our Insights page.

What are super apps in Vietnam's context? + –

Super apps in Vietnam are comprehensive mobile platforms that combine multiple services into a single application. These apps, such as MoMo, ZaloPay, and VNPay, offer everything from mobile payments and money transfers to insurance, investments, and bill payments.

How big is Vietnam's mobile payments market in 2026? + –

As of 2026, Vietnam’s mobile payments market is valued at approximately US$40.5 billion. This substantial market size reflects the rapid adoption of digital payment methods across the country, driven by government initiatives, increased smartphone penetration, and the growing popularity of super apps among Vietnamese consumers.

What role does the State Bank of Vietnam play in digital transformation? + –

The State Bank of Vietnam serves as the central regulatory authority driving the country’s digital transformation agenda. It issues regulations, creates legal frameworks supporting financial inclusion, and oversees regulatory sandboxes that allow FinTechs to test innovations.

Why are QR code payments growing so rapidly in Vietnam? + –

QR code payments represent the fastest-growing payment segment in Vietnam as of 2026. This growth is driven by several factors: the SBV’s National Payment Strategy promoting QR code adoption, the convenience and low cost of implementation for merchants, widespread smartphone usage, and the integration of QR payment capabilities into popular super apps.

How has COVID-19 impacted Vietnam's shift to cashless payments? + –

The COVID-19 pandemic significantly accelerated Vietnam’s transition to cashless payments. The need for contactless transactions during the pandemic drove a surge in online and digital payment adoption. This shift enabled both state-owned commercial banks and FinTechs to address service gaps more effectively, expand their online product offerings, and better align with the preferences of tech-savvy consumers who increasingly prefer digital over cash transactions.